This post doesn’t break any news, but addresses a basic question: what is the difference between direct EB-5 and regional center EB-5?

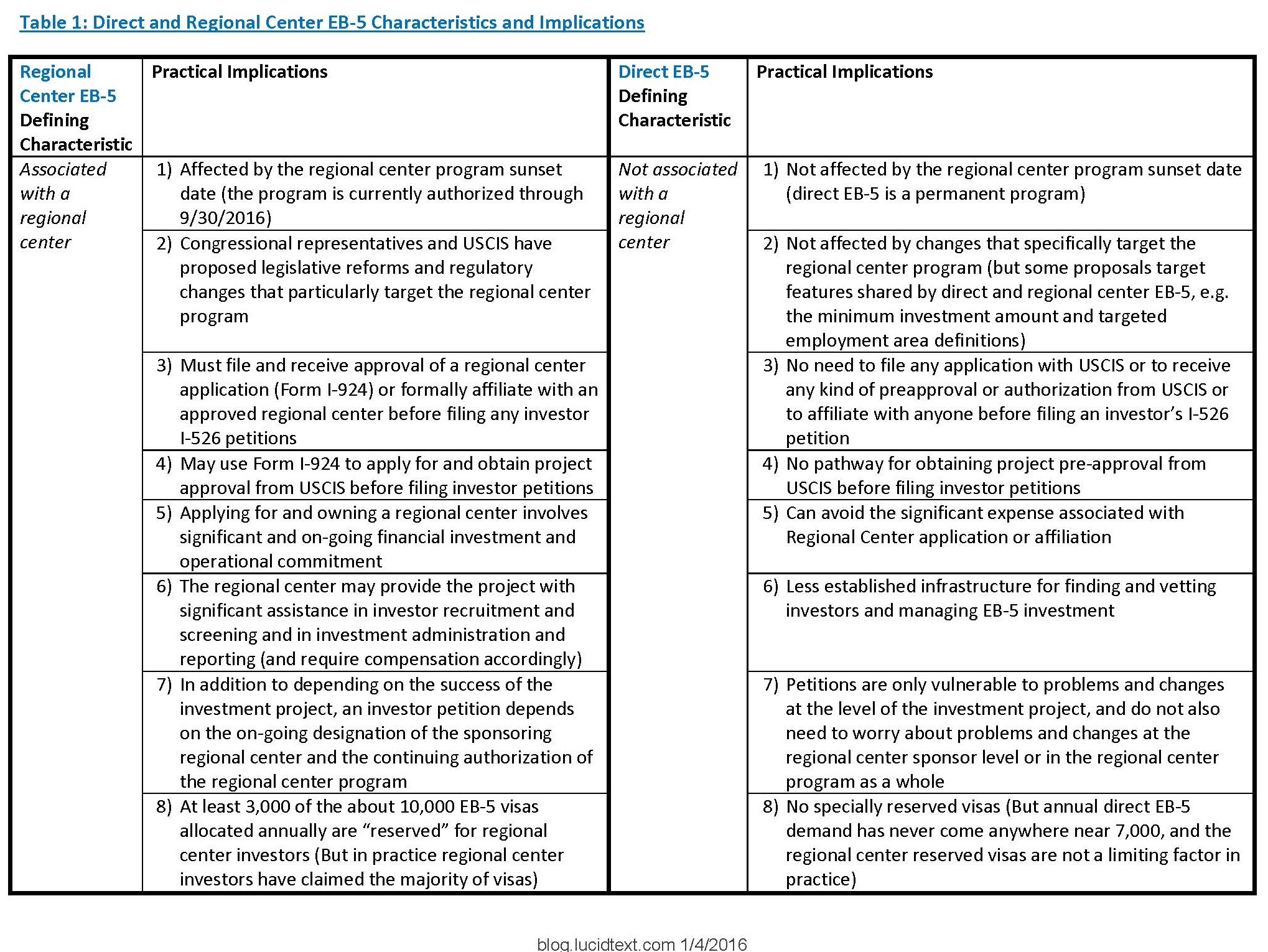

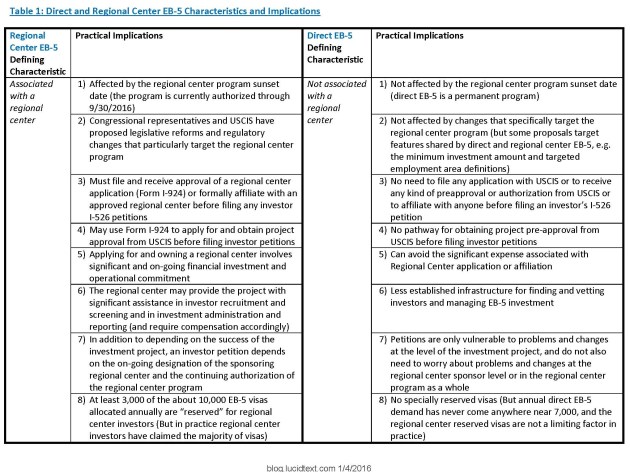

In a nutshell, the answer is that a regional center investment is associated with a designated regional center and therefore may count indirect job creation, while a direct EB-5 investment is not associated with a regional center and may not count indirect jobs.

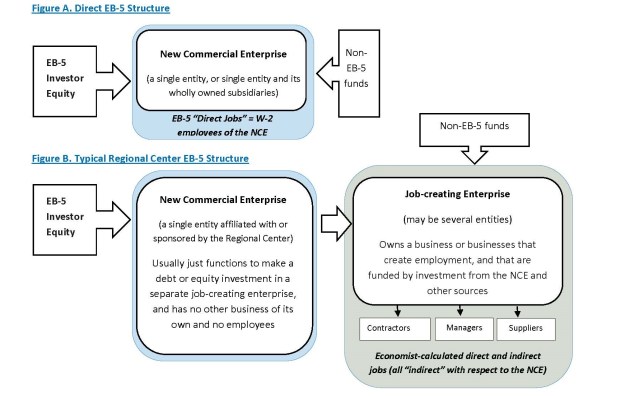

These two differences – regional center affiliation and indirect job creation – are the only fundamental differences between direct and regional center EB-5. The two tracks share the same basic EB-5 requirements: investment of capital in a new commercial enterprise that creates jobs. Contrary to popular misconception, direct and regional center EB-5 have the same minimum investment amounts, the same targeted employment area incentives, and (USCIS claims) about the same average petition processing times.

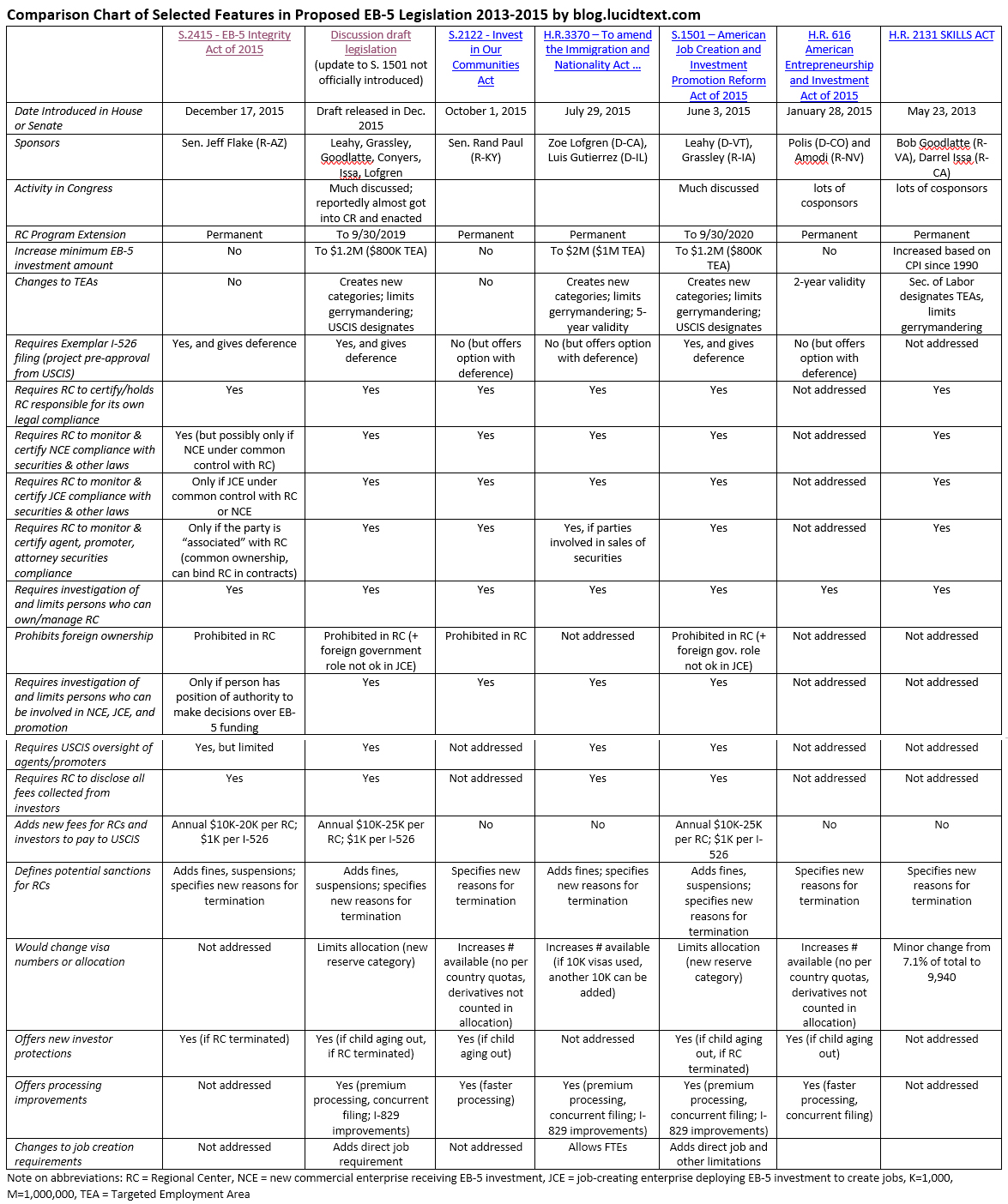

However, the two fundamental differences between direct and regional center EB-5 have implications that make direct and regional center investments quite different in practice. (Click on the images below to see full-size versions of the comparison charts, or click here for a PDF version.)

Examples

Some common scenarios will illustrate the differences, as described above, between direct and regional center investment:

- Real estate development projects are the most common investment for regional center EB-5 but awkward-to-impossible for direct EB-5. Indirect job creation allows the regional center investor in a landowner to count construction contractor jobs, indirect impacts of supply purchases, and sometimes even jobs created by the tenants of the completed development. A direct investor who invests in the same landowner could only count the permanent W-2 employees of the landowner – but normally the landowner wouldn’t have any employees. Most construction work gets done by employees of a variety of contractors, none of which “indirect” jobs count for direct EB-5, and any direct employee positions lasting only the duration of the construction project may also be disqualified because they are not permanent.

- Hotels are a common investment for both regional center and direct EB-5, but subject to different considerations. The regional center hotel investment has the luxury of segregating EB-5 investors in an entity that neither owns nor controls the hotel, but simply exists to raise EB-5 capital and make a debt or equity investment in the hotel. This entity can claim credit for hotel jobs, thanks to indirect job creation. Direct investors, on the other hand, can only get credit for direct jobs and so can’t be segregated, but must have equity interest in the hotel owner/employer. (This can bring up liability issues, and may mean that direct EB-5 investors have to be vetted as owners in the franchising and liquor license process.) It’s no problem for regional center EB-5 if one entity owns the hotel and a separate management company hires the hotel employees, since indirect job creation doesn’t take into account which name appears on payroll records. In direct EB-5, this is a problem. Direct EB-5 can’t separate investment from job creation, and therefore the entity that uses EB-5 capital to develop the hotel needs to be the same entity with new hotel employees on its payroll. (If multiple entities are involved in direct EB-5, they must be essentially united by a wholly-owned subsidiary relationship.) Furthermore, a hotel will be able to claim more job creation as a regional center project than as a direct project. A new-build 120-room Homewood Suites might subscribe two direct EB-5 investors based on a business plan anticipating creation of 23 full-time positions, or twelve regional center EB-5 investors based on an economist’s calculation that hotel construction and operation will result in 130 new jobs. Why are the two jobs numbers so different for the same hotel? First, the direct investor can only count hotel employees while the regional center investor can also count construction-associated jobs and economist-defined indirect and induced jobs (associated with supply purchases and employee spending). Second, the direct investor can only count payroll-record-verified full time positions, while an economic model is relatively generous in counting operating jobs. The economist’s multipliers are based on averages, cannot distinguish between full-time and part-time employment, do not consider who holds the jobs, and are not finely tuned to reflect labor variations among hotels of different flags and scales. The economic model calculates average direct employment for an average hotel with a given verified revenue, and this number usually exceeds the number of discrete, verifiable 35+ hour per week positions at an individual hotel. Finally, I-829 paperwork may be easier for the regional center investment than the direct investment. The hotel with direct investors needs to sign up for E-Verify, take special care that its employees are qualifying, maximize full-time employment, and prepare stacks of payroll records to verify job creation. The offering with regional center investors and an economic analysis using expenditure and revenue inputs can (in theory) not worry about individual employees but rather track expenditures and revenue, and prepare financial statements to verify employment by verifying economic model inputs.

- Small businesses such as restaurants and gas stations are likely to use direct EB-5. Such businesses tend to require only a couple EB-5 investors and will have sufficient direct jobs to justify those investors without needing to rely on indirect job creation. They can generally accommodate EB-5 investors as equity members and don’t require the complex investment structures only possible for regional center EB-5. No regional center affiliation means no regional center fees, no geographic limitation, and no vulnerability to regional center program changes. Regional center investment could work for these projects too and has the attraction of flexibility. But these projects may not be attractive to regional centers, which are often unwilling to sponsor offerings that only need a couple investors, and direct EB-5 provides a viable alternative.

- Investments involving multiple layers and diversification can work in the regional center context but not for direct EB-5. If a direct EB-5 case has multiple entities in the flow of EB-5 capital or in the staffing plan, then those entities must be united by a wholly-owned subsidiary relationship. If they aren’t so related, then the case will be denied. For example see OCT022015_01B7203 Matter of H-G- (direct investment in a new commercial enterprise that invests in a separate job-creating business), NOV122014_01B7203 and DEC042013_01B7203 (direct investment and job creation divided among several enterprises), JUN182013_01B7203 and JUN042013_01B7203 (job creation in partially-owned subsidiaries).

Regulatory Background

What rules underlie the practical differences between direct and regional center EB-5? To quote the EB-5 Policy Memo: “The EB-5 Program is based on three main elements: (1) the immigrant’s investment of capital, (2) in a new commercial enterprise, (3) that creates jobs.” Direct and regional center EB-5 investors share these elements and the requirement to contribute capital (equity not debt) to a (single) new commercial enterprise and create jobs. The difference comes in term definitions. “Employee” for a direct investor can only mean “an individual who provides services or labor for the new commercial enterprise and who receives wages or other remuneration directly from the new commercial enterprise.” The word has an additional sense for the regional center investor: “an individual who provides services or labor in a job which has been created indirectly through investment in the new commercial enterprise.” The EB-5 regulations at 8 CFR § Sec. 204.6(e) define terms:

- Commercial enterprise means any for-profit activity formed for the ongoing conduct of lawful business including, but not limited to, a sole proprietorship, partnership (whether limited or general), holding company, joint venture, corporation, business trust, or other entity which may be publicly or privately owned. This definition includes a commercial enterprise consisting of a holding company and its wholly-owned subsidiaries, provided that each such subsidiary is engaged in a for-profit activity formed for the ongoing conduct of a lawful business. This definition shall not include a noncommercial activity such as owning and operating a personal residence.

- Employee means an individual who provides services or labor for the new commercial enterprise and who receives wages or other remuneration directly from the new commercial enterprise. In the case of the Immigrant Investor Pilot Program, “employee” also means an individual who provides services or labor in a job which has been created indirectly through investment in the new commercial enterprise. This definition shall not include independent contractors.

- Invest means to contribute capital. A contribution of capital in exchange for a note, bond, convertible debt, obligation, or any other debt arrangement between the alien entrepreneur and the new commercial enterprise does not constitute a contribution of capital for the purposes of this part.

For additional discussion see my Direct EB-5 Page.