Regional Center Program Authorization History and FAQ

June 8, 2026 2 Comments

The regional center program was established as a “pilot program” back in 1992, and has had 35 extensions since then. The current program authorization extends through September 30, 2027. This post addresses FAQ around authorization status and explains how authorizations happened historically.

I wrote this post months ago, then held off on publishing because the issue can seem moot. Does regional center reauthorization matter, when the government is busy trying to scare off immigrants and visa numbers are insufficient to underwrite ongoing demand? But I keep encountering questions and misconceptions about the 2026 and 2027 EB-5 deadlines (including from AI, which threw up a festival of hallucinations when I asked about regional center authorizations). So, drawing from the library I’ve assembled over the past 16 years, here is an article with reliable FAQ.

Is the EB-5 program set to expire?

No, EB-5 is not set to expire. The EB-5 category is as permanent as EB-1 to EB-4, and does not need to be reauthorized. Temporary authorization is specific to the regional center program within EB-5. If the regional center program expires, then what remains for new investors will be the standalone direct EB-5 option. Direct EB-5 allows single EB-5 investments resulting in verifiable payroll jobs. It lacks the regional center distinctives of indirect job creation and pooled EB-5 investment. (Reference: USCIS Policy Manual)

Are EB-5 visa categories or visa numbers set to expire?

No, EB-5 visa categories are not set to expire. EB-5 visas are attached to the EB-5 program, which has no set sunset date. Reserved visas for rural, high unemployment, and infrastructure are part of the law for EB-5 generally (INA 203(b)(5)(B)), not a subset of the law that is specific to regional centers. Future law could change EB-5 visa allocation (as happened before in 1997 and 2022), but the current set-aside categories are not set to expire on any given date. (As a practical matter, only regional center investors can qualify for Infrastructure visas. But the Infrastructure visa set-aside is not, itself, theoretically contingent on ongoing RC program authorization.)

Can today’s regional center investors count on future access to EB-5 visas, no matter what happens? What investor protections exist in case the regional center program expires?

There are qualifications around how regional center investors can access EB-5 visas.

The law specific to regional centers in Subsection E of INA 203(b)(5) currently simply states that “visas under this subparagraph shall be made available through September 30, 2027.” Thankfully, Subsection S of INA 203(b)(5) adds some grandfathering protection for people still in process as of 2027. Subsection S indicates that even if the authorizing legislation referenced in Subsection E expires, the government should continue processing I-526E and I-829 petitions, not deny petitions simply due to program expiration, and “not suspend or terminate the allocation of visas to the beneficiaries of approved petitions.”

Subsection S specifies that “protection from expired legislation” only applies to petitions “associated with a regional center that were filed on or before September 30, 2026.” Note that the regional center grandfathering protection deadline is one year earlier than the regional center program sunset date. (This may have been a typo, but anyway it’s the law now.)

The grandfathering language in INA 203(b)(5)(S) is specific and narrow. It does not protect investors from every change that might happen during their immigration process, or from every side effect in case of expired legislation. But it tries to specify that – at least – a future regional center program lapse would not halt processing and visa issuance for in-process regional center investors.

Is regional center grandfathering protection important? Not if one can count on reauthorization. For a couple decades in EB-5, we didn’t feel the lack of this protection. But if there’s a question or a lapse, the protection becomes critical. Just ask any regional center investor who did not have a visa yet in 2021, and lived through the extended regional center program lapse that started in July 2021. USCIS stopped processing regional center petitions, and Department of State stopped issuing visas to regional center applicants. Both agencies interpreted that loss of program authorization prevented any in-process regional center investors from moving forward. There was question as to when and if the program would ever get reauthorized. Months dragged on. USCIS threatened a deadline to stop holding regional center petitions in abeyance, raising the specter of mass denials due to loss of program authorization. Many grey hairs resulted. The investor association AIIA was created to fight for a fix for this distressing situation. Their lobbying thankfully resulted in such grandfathering protection as exists for investors through September 2026.

Some grandfathering protection from expired legislation exists on the government side. Regional centers and investors should still consider the plan for sponsors to stay in business and fulfill their ongoing administrative and reporting requirements, even if a lapse cuts off the flow of revenue from new investors.

Does Regional Center program reauthorization typically come with significant EB-5 changes?

Historically, regional center program extensions have not been packaged with other EB-5 changes. The only wide-ranging EB-5 legislative changes in history are the EB-5 Reform and Integrity Act of 2022 in PL 117-103, and three pages of EB-5 reform provisions included in PL 107-273 back in 2002.

The majority of past regional center authorizations consisted of only this one sentence, tucked somewhere in an annual appropriations act without other EB-5 provisions: “Section 610(b) of the Departments of Commerce, Justice, and State, the Judiciary, and Related Agencies Appropriations Act, 1993 (8 U.S.C. 1153 note) shall be applied by substituting [date] for [date].”

Should regional center program reauthorizations come with significant program changes? Congress and industry battled over this question for most of the last decade, and it remains an open question.

How did the regional center program get reauthorized in the past?

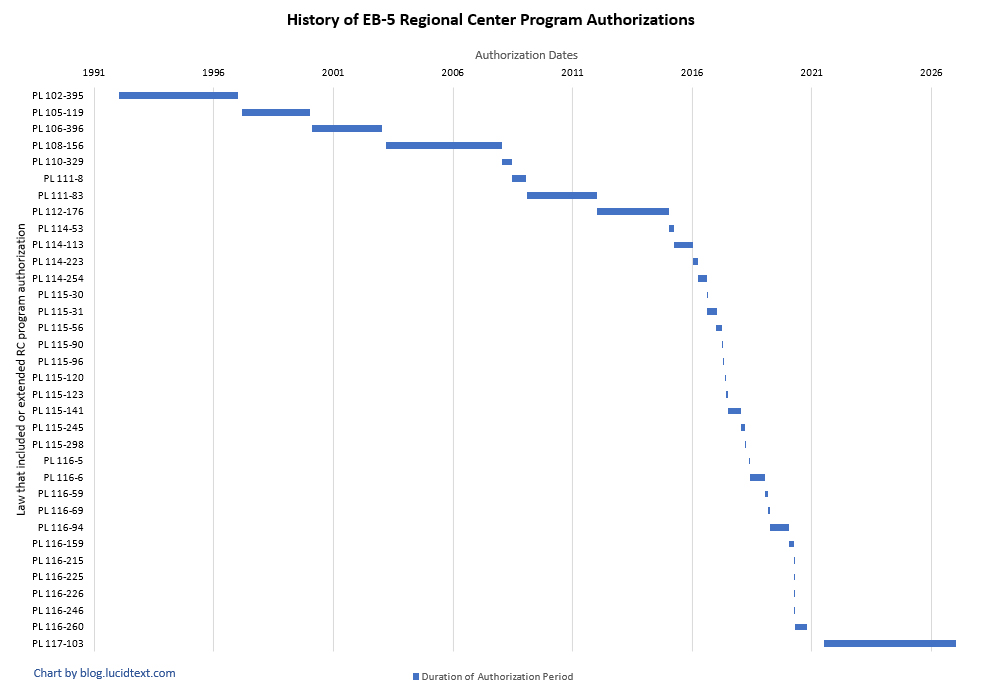

As usual, I have an Excel file for that. My log of past regional center program authorizations gives the title for each law behind past authorization extensions, together with notes on context, duration, and content. The following scary chart visualizes the reauthorization history.

And here is a summary of the reauthorization history in words, to provide context.

1993-2009: Multi-year regional center authorizations were shepherded by program champion Senator Leahy, without much controversy for a low-profile and lightly-used program. Senator Leahy sponsored or co-sponsored most bills behind reauthorization in this period.

2010-2015: Senator Grassley became an active player with Senator Leahy in EB-5 discussions. Reform talk heated up following robust post-recession program growth and a couple high-profile scandals. Regional center program authorization got linked with three other immigration programs that needed regular extension, including E-Verify – possibly helping RC authorization by making it less individually controversial. 2012 was the last time that RC authorization happened in standalone immigration legislation, rather than tucked into a funding bill (an Omnibus or Continuing Resolution for appropriations).

2015-2020: This period was characterized by fragmented regional center program authorizations, each lasting just a few months. Coupling with the annual appropriations process had pros and cons. On the one hand, it’s practically much easier to simply insert or preserve one sentence in a multihundred-page bill than to get a stand-alone bill passed for an issue. On the other hand, the appropriations timeline is a mess. Whenever Congress could not agree on a funding bill, then RC authorization also suffered by default, for lack of vehicle. Fragmented RC program authorization dates during this period mirror the broken pattern of dates for annual appropriations acts, continuing resolutions, and funding lapses. Another factor in this period was the struggle between a “mend it” faction (spearheaded by Senator Grassley and Senator Leahy, who now wanted to see any regional center reauthorization accompanied by significant EB-5 reforms) and a “keep it” faction (pushed by some regional centers and facilitated by Senator Schumer, wanting to maintain a status quo of reauthorization without disruptive changes). Many competing EB-5 bills were proposed, hearings were held, and back-room fights raged every year. Do a key word search for “EB-5” on Senator Grassley’s website if you’d like an earful of the drama from this period.

2021-2022: The “mend it” faction finally came out on top in 2021 by getting the RC program authorization a mid-year expiration date, thus de-coupling it from annual appropriations. An extended program lapse resulted, and caused pain that finally pushed agreement on a version of the Grassley/Leahy reform bill that became the EB-5 Reform and Integrity Act of 2022 (RIA). All prior regional center authorizations had added time to the original 1993 pilot authorization. RIA repealed the 1993 authorization, and codified the regional center program in the INA.

2022-today: Dynamics are changing in the regional center industry and in government. The EB-5 issues that caused big legislative fights from 2010 to 2020 were largely settled by the extensive reforms enacted in 2022. Senator Leahy, who originally championed the regional center program and lead the critically-important Senate Judiciary committee for most years between 2001 and 2015, is no longer in Congress. Senator Grassley remains well-placed for now, with EB-5 at least somewhere on his busy radar. There’s a case that the RC program is functioning as Congress intended, with integrity measures in place and billions invested in rural areas. We witness the environment in Washington these days, the rhetoric around immigration, and how good Congress is at passing legislation on time – especially funding bills. I deleted adjectives from that sentence, judging appalling, horrific, and dire not quite strong enough. We can guess about future shifts with coming elections, and guess how EB-5 may rank among legislative priorities.

How likely is the regional center program to be reauthorized past September 30, 2027?

I will let you make your own assessment of reauthorization prospects. History shows that legislative action can effectively depend on just a few motivated people. Also, that past performance was driven by factors that are mostly changed today, or about to change. For those with a stake in the regional center program, a better question might be: What can I do to support the chance of reauthorization? Regional center association IIUSA and investor association AIIA would welcome support. This is not an easy process, and advocates are needed.