Facing FY2023, Suggested Articles, October 2022 Visa Bulletin

September 30, 2022 11 Comments

Today marks the end of Fiscal Year 2022, and the first September since 2015 that I haven’t spent reporting on Congressional news and the appropriations process, waiting with bated breath for updates about regional center program authorization.

Thanks to the EB-5 Reform and Integrity Act of 2022, we now have until September 30, 2027 to panic about legislation to reauthorize the regional center program. EB-5 is stable today in the sense that it neither requires nor anticipates near-term legislative action.

My dream for the future is that EB-5 will also stabilize in the sense of offering a reliable opportunity to immigrate based on investment. In this dream, investor petitions will be processed. Policy will be written. Adjudications will be based on transparent standards, and will have a predictable timeline. Visa availability will be transparent and predictable. Investors who satisfy all the requirements will get a chance to immigrate before they age out, give up, or die. An investment will be an investment, not an unpredictable series of deployments. Escrow protection will be possible. Regional centers will know where their status and responsibilities begin and end. EB-5 issuers will be constrained to make offerings that can and do bear scrutiny as investments. Reasonable exit strategies will be expected and possible. The experience of existing investors will influence a regional center’s ability to attract new investment. Good actors will be empowered to plan well based on good information about the immigration process and success factors. Bad actors will not flourish in impunity underwritten by long processing queue times, policy uncertainty, misdirected adjudication, and lack of communication from USCIS. Both the government and stakeholders will put stock in what happens after investors make investments and file petitions. We’re partway there, and with so much scope for improvement going forward.

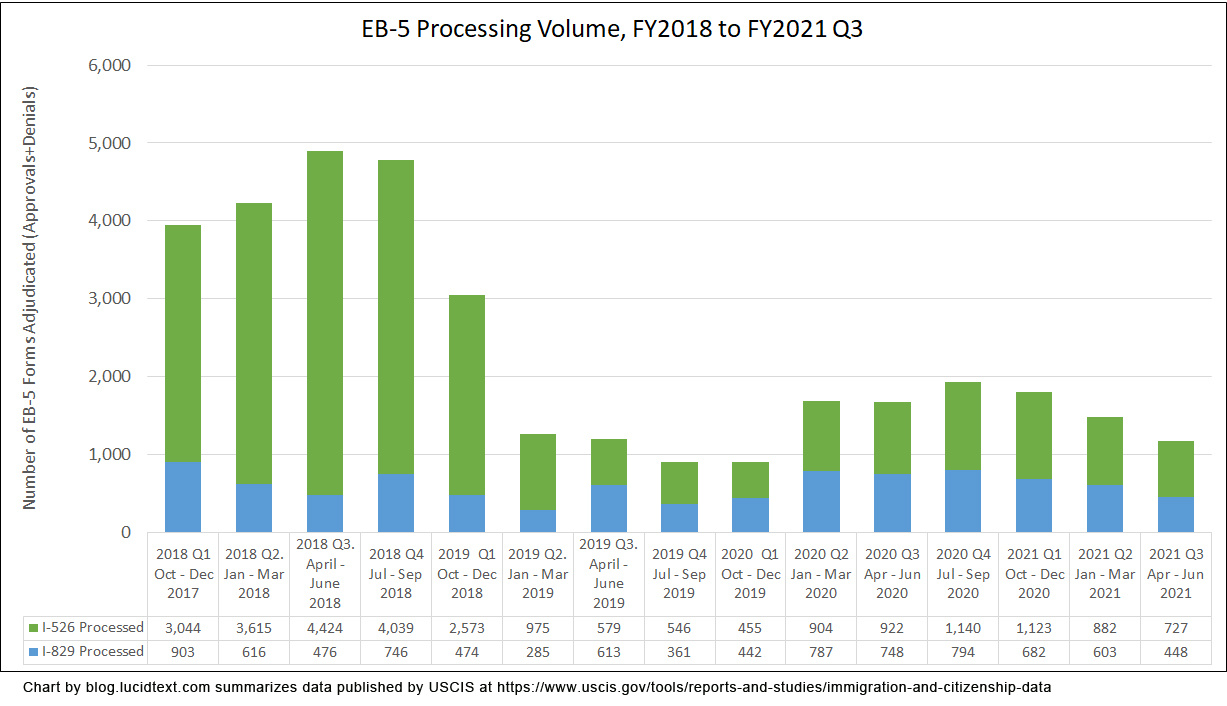

To the extent that words can help, I hope and plan to bring out articles on FY2023 visa availability and reserved visas implementation, the scope of exemplar approval, denial factors and issues for attention in IPO adjudications, questions about regional center and investor status after December 29, China timing factors, India timing factors, market size potential and constraints, issues and questions in new forms, and changing project success factors in the wake of the new law. In the meantime, I’ll suggest a reading list of articles from other sources, followed by a comment on the October 2022 visa bulletin.

Reading list:

- Fiscal Year 2023 Employment-Based Adjustment of Status FAQs” (09/08/2022) at USCIS.gov. A detailed and informative Q&A from USCIS about the specific processes involved in employment-based visa allocation. Predicts the number of FY2023 EB visas available, settles a question about EB-5 visa carryover, and offers valuable practical tips for I-485.

- Reserved Visa Rules, Possible Future Visa Allocation, and Recommendations” (09/09/2022) on the IIUSA blog. Written by Joseph Barnett and Lee Li in consultation with Charles Oppenheim, this article provides clear and updated analysis on reserved visas. The article revised my understanding, particularly with respect to how reserves interact with country caps. Once I get feedback from the authors on a couple points, I’ll publish a revision to my article from April.

- IIUSA Questions and Comments for October 19, 2022, EB-5 Stakeholder Engagement (09/16/2022) IIUSA did nice work in articulating many pain points in IPO operations, pointing out why the problems are problems, and suggesting feasible solutions. Now that someone has done all the work to write out these good comments, let’s all read them and amplify them with repetition. (Also FYI, here are the comments I submitted to USCIS, focused on my top concerns of transparency, and the status of pre-RIA regional centers and investors.)

- IIUSA Teams Up with Kurzban Kurzban Tetzeli & Pratt to Seek USCIS Records on EB-5 Source of Funds Adjudications (9/7/2022) on the IIUSA blog. This article reports on one step in a very important battle: taking on the new USCIS practice of denying I-829 over source and path of funds that were approved at the I-526 stage. I’m glad to see this critical issue getting attention and action.

- How long must you keep EB-5 capital at risk? (9/27/2022) in EB5 Investors Magazine. Robert Divine explains how the EB-5 Reform and Integrity Act changed the EB-5 sustainment period, and the consequences for new investors and redeployment. This is game-changing good news, if USCIS also sees what Robert sees in the law. Another point worth amplifying.

I considered writing an article about the October 2022 Visa Bulletin, discussing what it means for demand to “materialize,” as the visa bulletin notes like to say. Also, pointing out which applicants the visa office accounts for in setting monthly visa bulletin dates, which applicants (by contrast) we need to account for in estimating visa wait times, and what all that means for predicting future action dates. But instead, I made a picture. I hope that just looking at this image can help conceptually. After examining the picture, you may want to consult this presentation and my data summary for most recent available estimates of the number of applicants hidden in the EB-5 process clouds (not yet on the Visa Control radar, but important for us because determinative for future visa bulletins). And then if you still really wish you had an article about the Visa Office perspective behind visa traffic control, I recommend Note F in the November 2021 Visa Bulletin, this article, and the Chat with Charlie for the April 2021 visa bulletin.