Final Fee Rule, Processing Updates, RC Withdrawal

October 24, 2016 1 Comment

Today the Federal Register published U.S. Citizenship and Immigration Services Fee Schedule, a final rule adjusting the fees required for most immigration applications and petitions. USCIS invites stakeholders to participate in a Fee Rule Engagement teleconference on November 2, 2016 from 3:30 to 4:30 PM EST. (To register, click on the USCIS registration page.)

The final rule is similar to the proposed rule that we reviewed this summer, with the addition of DHS response to public comments. Here are the portions of the rule particularly significant to EB-5 (summarized from PDF pages 17-20, 30-31, and 41 of the final rule).

Fee Increases

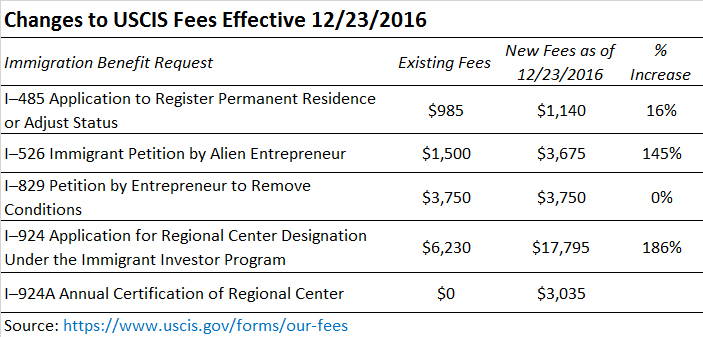

EB-5 petitions and applications become more expensive to file as of December 23, 2016.

The fee increase for Form I-924 is especially drastic, and I’m surprised to discover that USCIS apparently did not hear public feedback on its two most obvious problems: that it was assessed based on inaccurate assumptions about regional center revenue, and that it will discourage regional centers from voluntarily using I-924 to file the amendment requests and Exemplar I-526 that USCIS wants to encourage. IIUSA and AILA – did you drop the ball on commenting, or did USCIS just not pay attention? But the rule is final now, so we live with it. And Regional Centers, you might want to hustle to file any exemplars and amendments before December 23.

Processing Issues

- The rule does not promise that fee increases will bring improved service for EB-5 petitions. The rule states that higher fees will be used to recover costs needed to sustain current operating levels, pay a share of services that DHS provides on a fee-exempt basis to others, bolster IPO’s fraud detection and national security capabilities, and make limited investments in technological improvements to bolster information security. These uses have merit, but none are directly linked to improved EB-5 processing times. But the rule does claim that the new I-924 fee “was, in part, calculated to allow USCIS to hire additional staff to process Forms I–924 and provide better and more thorough service.”

- The rule includes in passing this interesting tidbit on how IPO currently handles I-829 adjudications:

DHS appreciates the suggestions for improving EB–5 processing times. DHS clarifies that USCIS already has processes in place to streamline adjudication of the business-related portions of multiple Forms I-829 associated with a single, new investment project. Specifically, when USCIS receives a regional center-associated Form I–829 that involves a new commercial enterprise, USCIS reviews the first two petitions associated with that new commercial enterprise to determine if there are specific project-related issues that would apply to all petitioners associated with the new commercial enterprise. After completing that review, USCIS commences adjudication of all Forms I–829 associated with that new commercial enterprise filed within a given period. Similarly, when USCIS receives a regional center-associated Form I–829 that involves a previously reviewed commercial enterprise, USCIS immediately assigns that petition for adjudication. In other words, USCIS currently adjudicates Form I–829 petitions in ‘‘first in, first out’’ order by new commercial enterprises.

- The rule gives the welcome news that “USCIS is transforming how it calculates and posts processing time information to improve the timeliness of such postings, but more importantly, to achieve greater transparency of USCIS case processing.” To that end, “USCIS is evaluating the feasibility of calculating processing times using data generated directly from case management systems, rather than with self-reported performance data provided by Service Centers and Field Offices” and “USCIS is also considering publishing processing times using a range rather than using one number or date. This approach would show that, for example, half of cases are decided in between X and Y number of months.” (Or, as Sir. Humphrey Appleby might say: of course we understand that you want a usable processing report, and have convened an interdepartmental committee to conduct a feasibility study that will make recommendations at the appropriate juncture, in due course, when the moment is ripe, in the fullness of time. Rome wasn’t built in a day.)

- The rule says that “USCIS does not have immediate plans to allow electronic filing for EB–5 requests, but appreciates commenters’ desire to avoid voluminous paper filings. USCIS plans to allow electronic filing for EB–5 requests in the future.”

Regional Center Withdrawal Procedure

The rule recognizes the problem that “Currently, there is no procedure for regional centers seeking to withdraw their designation and discontinue their participation in the program,” and offers to provide a withdrawal procedure to “allow a regional center to proactively request withdrawal without the need for the more formal notices sent out by DHS.” To this end, the rule amends the EB-5 regulations, replacing 8 CFR 204.6(m)(6) with the text I quote below. The new language is similar to the previous 8 CFR 204.6(m)(6) except that it adds failure to pay fees as a reason for termination and adds a rather vague paragraph stating that a regional center may notify USCIS by letter or other means if it wishes to withdraw from the program. The paragraph does not clarify what the letter should include, where it should be sent, what kind of decision USCIS has to make about the letter, and to what extent such a regional center will be treated differently from another whose designation is terminated involuntarily.

PART 204—IMMIGRANT PETITIONS

■ 8. Section 204.6 is amended by revising paragraph (m)(6) to read as follows:

- 204.6 Petitions for employment creation aliens.

* * * * * (m) * * *

(6) Continued participation requirements for regional centers.

(i) Regional centers approved for participation in the program must:(A) Continue to meet the requirements of section 610(a) of the Appropriations Act.

(B) Provide USCIS with updated information annually, and/or as otherwise requested by USCIS, to demonstrate that the regional center is continuing to promote economic growth, including increased export sales, improved regional productivity, job creation, and increased domestic capital investment in the approved geographic area, using a form designated for this purpose; and

(C) Pay the fee provided by 8 CFR 103.7(b)(1)(i)(XX).

(ii) USCIS will issue a notice of intent to terminate the designation of a regional center in the program if:

(A) A regional center fails to submit the information required in paragraph (m)(6)(i)(B) of this section, or pay the associated fee; or

(B) USCIS determines that the regional center no longer serves the purpose of promoting economic growth, including increased export sales, improved regional productivity, job creation, and increased domestic capital investment.

(iii) A notice of intent to terminate the designation of a regional center will be sent to the regional center and set forth the reasons for termination.

(iv) The regional center will be provided 30 days from receipt of the notice of intent to terminate to rebut the ground or grounds stated in the notice of intent to terminate.

(v) USCIS will notify the regional center of the final decision. If USCIS determines that the regional center’s participation in the program should be terminated, USCIS will state the reasons for termination. The regional center may appeal the final termination decision in accordance with 8 CFR 103.3.

(vi) A regional center may elect to withdraw from the program and request a termination of the regional center designation. The regional center must notify USCIS of such election in the form of a letter or as otherwise requested by USCIS. USCIS will notify the regional center of its decision regarding the withdrawal request in writing.