Reauthorization

There seems to be optimism that Congress and President Trump will agree before February 15 on a deal to fund the government for 2019. I assume and trust that the deal, when unveiled, will include extension of regional center program authorization at least to September 30, 2019. [Update: H.J.Res 31, which became law on 2/15, has regional center program authorization to 9/30/2019 in Division H, Title 1, Sec. 104 (PDF page 463), and no other changes that affect EB-5.]

Luckily for EB-5, the case against it has been taken up by the pariah Rep. Steve King. Last month he introduced H.R.773 – To terminate the EB-5 program, proposing that EB-5 be erased from the INA, and that DHS cease to accept new petitions and dismiss all pending petitions and applications. The bill has gained 0 cosponsors, reflecting what other lawmakers think of this proposal and/or of supporting anything associated with Steve King.

Visa Availability

The per-country cap for EB visas continues to be an issue in the new Congress, with at least two new bills proposing to eliminate it: H.R. 1044 ‘Fairness for High-Skilled Immigrants Act of 2019 and S.386 – A bill to amend the Immigration and Nationality Act. These bills have quite a few cosponsors. This time around, IIUSA has taken a stand on the issue. “While the elimination of per-country caps may make sense for some categories, the elimination of the per-country caps for EB-5 will be to the detriment of the program,” stated IIUSA Executive Director Aaron Grau. [2/18 Update: IIUSA has expanded on its statement. 7/1/2019 Update: See my post on Country Cap discussion.]

EB-5 Activity at USCIS

Here’s what USCIS has done publicly so far for EB-5 in 2019:

- Not finalized EB-5 regulations (or at least, not yet advanced them to OMB for review)

- Not approved or terminated any regional centers

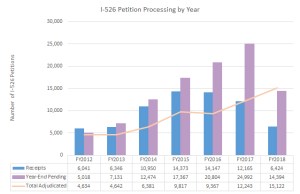

- Not published petition processing data for July-Sept 2018 (I expected this to happen by December 2018)

- Not held or announced any stakeholder engagements

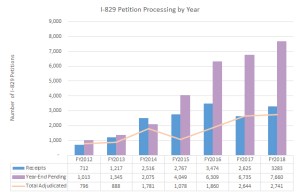

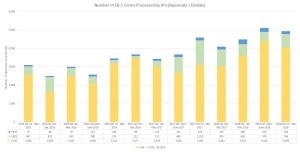

- Made a couple tweaks to petition processing time reports, each time adding or subtracting a few days. Currently, petitioners can be considered “outside normal” processing times if they are 796 days from I-526 filing, 1,077 days from I-829 filing, or 715 days from I-924 filing. Dear me. However, I’m hearing anecdotally of I-526 adjudicated within a year.

- Published a number of AAO decisions on EB-5 appeals (a few of which I discuss below)

Material Change and Redeployment

I have something to add to the redeployment discussion, as a business plan writer who has spent years grappling with the intersection of EB-5 theory and business practice. But until I have time to actually write the post I have in mind, here FYI are two planks to my thinking on the redeployment issue:

- Carolyn Lee’s analysis of the EB-5 at-risk requirement and its misapplication in redeployment policy. USCIS, be sure to read this article, which helps explain why applying redeployment policy is so hard for us. When a policy makes sense theoretically, then we don’t have to badger you with questions about how to apply it. Then we can figure it out ourselves with reference to the statue/regs/precedents etc., with the help of our smart lawyers. As it is, we do hassle you with questions because there’s a broken link to the established rules, giving us and you no firm foundation to stand on in applying the policy, and leaving us all vulnerable to capricious case-by-case determinations.

- A number of redeployment complications and constraints arise from the fact that redeployment policy is a subset of the material change policy. In preparation to discuss that aspect of redeployment, I’ve refreshed my post What is Material Change. The post discusses the theory and links to most AAO decisions that have addressed material change in specific cases.

USCIS decision-making

AAO decisions on EB-5 appeals shed light on an important question: “If anything goes wrong with an EB-5 investment, is there any way to recover?” What if a principal goes rogue and makes off with some funds, but then there’s new management and funds are recouped and put to work again? What if a regional center was terminated, but currently well-placed to promote economic growth? What if a project did not develop as originally anticipated, but can succeed and create jobs in a new direction? These questions fall in policy grey areas, giving the agency leeway for positive flexibility or reflexive naysaying. Unfortunately, recent AAO decisions show the later trend, and I hope that there will be pushback.

DEC102018_06B7203 Matter of L-X- is one of two decisions on appeal by investors who put money into an NCE originally managed by Emilio Francisco, who was charged by the SEC in December 2016 with defrauding investors. The NCE and other defendant entities went into receivership, it was determined that a portion of EB-5 investor funds had been diverted, and USCIS denied I-526 petitions for NCE investors. In an attempt to salvage the situation, several EB-5 investors executed an LOI with an institutional investor and amended the NCE’s LP agreement to replace the NCE manager, remove the NCE from receivership, provide necessary funding to the NCE, and complete and operate the project. USCIS/AAO claimed to be “sympathetic to the Petitioner’s situation,” but claimed that the investors still could not satisfy EB-5 requirements. Here’s the USCIS/AAO reasoning:

- The petitioner could not satisfy the “at-risk” requirement if she replaced diverted capital with additional investment, because that new capital would not be her original capital, and Izummi requires showing that the full amount of “original capital” was made available to the NCE to create jobs. “Petitioner must establish the necessary job creation with capital invested at the time of filing, not based on later infusion of additional funds.” (I don’t quite follow the justification from Izummi, or the “original capital” idea generally. Is the thought that the very dollar bills first passed between the investor and NCE must be the same dollar bills used to pay employee salaries? USCIS sometimes talks about a “path of funds” from investment to job creation – as if cash flowed through a business with each note radio-tagged and leaving a colored path as it goes. In practice, investment goes together into a pool and economic activity and jobs and ROI come out of the pool. A “path of funds” from X original dollar to Y job never exists, and USCIS/AAO should not make demands that presume such a path.)

- If the investor replaced $182,133.33 of diverted capital with $182,133.33 in additional investment, then the petitioner would be committing impermissible material change because that would effectively increase the minimum investment amount from $500,000 to $682,133.33. (Really, USCIS? How does investing more than the required minimum undermine eligibility?)

- USCIS couldn’t tell whether the Petitioner had actually invested the additional funds, or only intended to do so. (This is a fair point, but why did USCIS raise this issue if against additional investment in principle?)

- The Petitioner did not demonstrate that all approvals needed for the proposed NCE restructuring had been obtained, making USCIS doubt whether the restructuring could go forward. (Fair point, if true.)

- The Petitioner did not file an updated business plan to describe the current status of the project and its current job creation potential. (I wonder if this was fundamentally the most important problem with the Petitioner’s appeal. A business plan is a chance to tell a compelling story about use of investment and job creation, reconcile apparent inconsistencies, argue that changes aren’t material, make an eligibility case, and pre-emptively address questions, doubts, and misconceptions that the reader might have. Don’t miss the prime opportunity to tell your story! As a business plan writer, I’m sensitive to the critical and delicate role of the business plan in presenting changed circumstances to USCIS.)

DEC042018_01K1610 Matter of P-A-K is AAO’s third decision regarding the designation of Path America KingCo regional center. This decision was compelled by US District Court, where the regional center filed a complaint after the AAO denied its initial appeal and motions to reopen and reconsider. AAO gives 21 pages this time to reiterate the denial, with arguments that can be summed up in this sentence that the decision quotes from INS v. Abudu: “The INS should have the right to be restrictive.” Path America KingCo presents a compelling case for its current and future potential to promote economic growth, but the AAO finds that this isn’t relevant to its current designation status. AAO rests on this technical claim: that appellate decisions are final, and cannot be reconsidered in light of new evidence, but only reassessed in terms of evidence that existed at the time the decision was made. One might think that Path America KingCo deserves designation if it is continuing to promote economic growth, but AAO says no – the relevant issue is whether it was promoting economic growth at the time it was terminated. A different agency might’ve looked at the fact pattern – a company that has good management (now), good projects, and committed investors dependent on the designation – and found a way to say yes. The so-called “balancing test” discussed in prior terminations claims that “we take into account a variety of factors, both positive and negative, that encompass past, present, and likely future actions.” However, it appears that this test does not apply on appeal, as USCIS does not consider positive present or likely future actions once a termination letter has been issued.

Letter to Senator Collins in the USCIS electronic reading room shows USCIS responding frostily to a plea from Senator Susan Collins regarding a small town in her constituency that planned to use EB-5 investment to rebuild after the catastrophic closing of a paper mill. The scenario sounds like textbook example of what Congress hoped EB-5 could do, but it did not move USCIS, which terminated the regional center purchased for the town before the town had a chance to use it, and just offered Senator Collins the cold comfort of filing an AAO appeal. Is this administering the Immigrant Investor Program in a fair and efficient manner? Fair and efficient, I suppose – the RC was apparently inactive prior to being taken over for Millinocket, Maine. But is the decision in tune with EB-5 program logic and objectives? No.

To be fair, AAO appeals sometimes work. JAN252019_01B7203 is an example of a denial that AAO remanded back to USCIS for more precision in identifying specific problems in credibility and eligibility, and for more rigor in assessing relevant evidence.

And as a reminder that court cases also sometimes work, EB-5 investors have another win on use of loan proceeds for EB-5 investment.