Today USCIS published form receipt and processing data for FY2024 Q2 (January to March 2024) on the USCIS Immigration and Citizenship Data page. I’ve updated my Processing Data page with all the FY24 Q2 EB-5 numbers, and provide charts in this post to highlight the big news.

New EB-5 filings skyrocketed in January to March 2024. Meanwhile, IPO took a large bite out of the EB-5 backlog with impressive productivity that recalls the good old days of 2018. We’re setting up for a busy and crowded time at the EB-5 visa windows in 2025 and beyond. (In other news, I’ve also updated my data repository with key visa-stage EB-5 numbers shared by Department of State at the IIUSA conference last month, to be discussed further in forthcoming articles. See IIUSA’s conference slides and a nice follow-up analysis by Lee Li that gives further detail and clarification.)

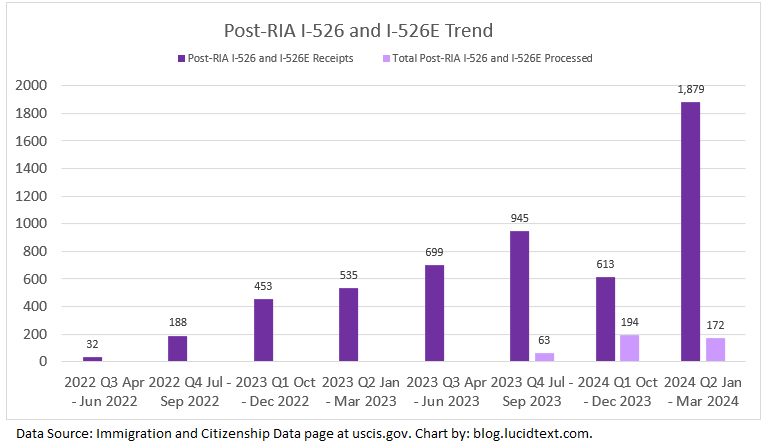

Post-RIA I-526 and I-526E Receipt Trend

USCIS reports that a whopping 1,810 I-526E and 69 I-526 were filed last quarter.

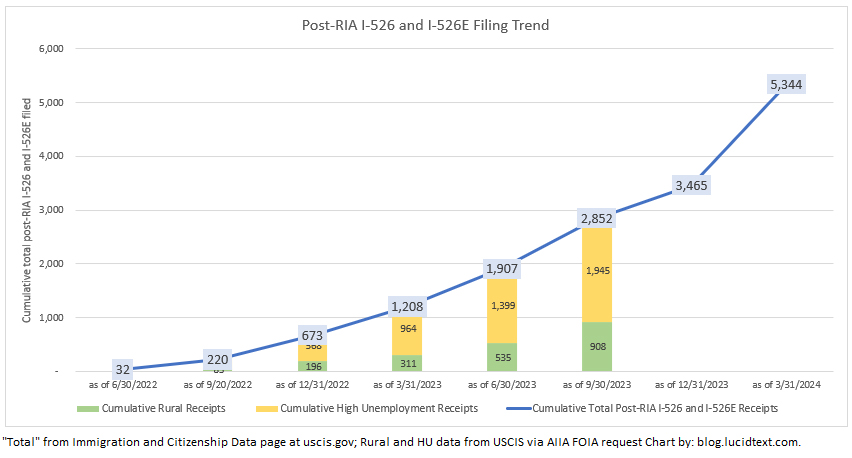

Counting up the quarterly reports from April 2022 (following the passage of RIA) to March 2024, we can see that USCIS has reported a cumulative total 5,344 post-RIA I-526 and I-526E filed, and 429 processed. (As a side note, the cumulative count conflicts with the FY24 Q2 period-end pending count. In the past, I’ve noted that the pending number ends up skewed after filing surges – I guess because last-minute end-of period receipts get counted as receipts in the period but only added to pending in the next period.)

In context, since RIA passed two years ago, EB-5 investors have brought at least 5,344*$800,000=$4.275 billion dollars into the U.S. economy. This investment was incentivized by the hope that approximately 5,344/.35=15,000ish visas will be available to these investors plus their spouses and children. (35% is an historical average of principals in EB-5 visas issued.) The number of post-RIA applicants who actually make it to an EB-5 visa will likely be significantly smaller due to country-specific variation and attrition, but the size of the upfront hope is impressive and sobering. Congress has not set aside sufficient annual visa numbers for this level of willingness to invest in economic growth and job creation. We don’t yet know how all I-526E filings break down by country or TEA category (AIIA has another FOIA request in progress for numbers since since November 2023), but this is a lot of prospective EB-5 visa applicants to fit in any lane, including Unreserved given the pre-RIA backlog. EB-5 visa advocacy should already be an urgent priority.

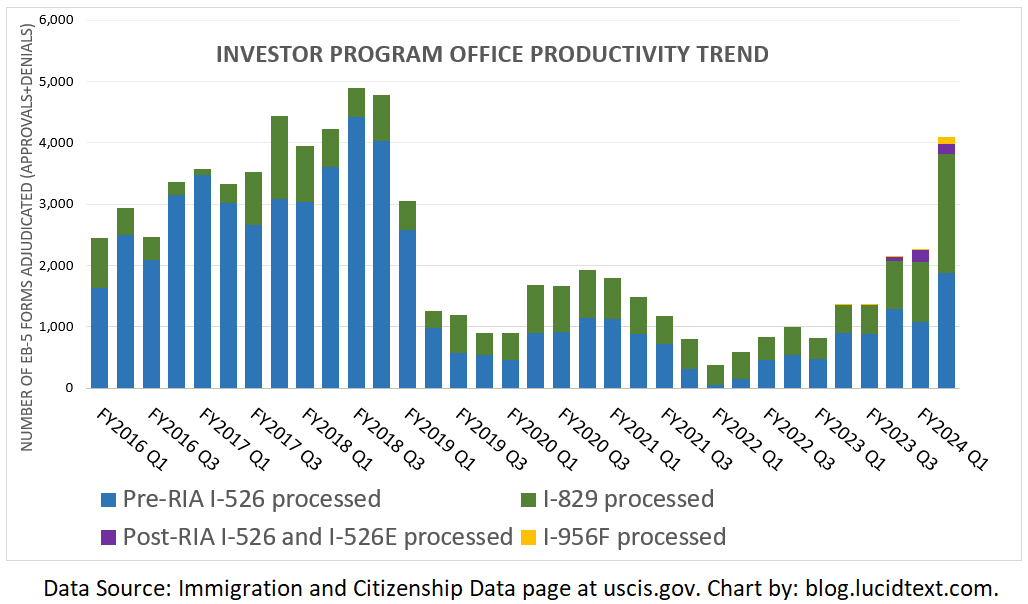

IPO Processing Productivity

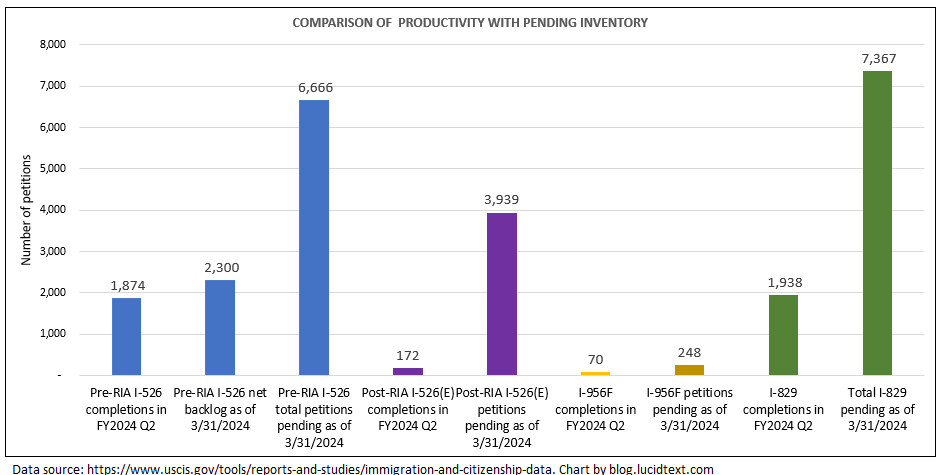

As I’ve been reporting based on unofficially obtained data, IPO has made a quantum leap in processing productivity. The first chart illustrates recent processing volume in historical context. The second chart compares FY24 Q4 processing productivity against the size of the backlog for select EB-5 forms. If IPO keeps processing at this rate, the pre-RIA I-526 and I-829 backlogs at USCIS will be gone within 12 months. And then adjudicators currently proving ability to turn out thousands of decisions per quarter will be able to shift focus and make quick work of the post-RIA inventory and incoming receipts. IPO still hasn’t published the RIA-required timely processing fee study, but even better it has gotten on track to actually realize the RIA timely processing goals in the foreseeable future.

How long do EB-5 funds stay invested? I’ve approached this hot question from several angles, including a previous blog post on the intersection between immigration timing and investment timing, and a webinar with CanAm and Robert Divine about the sustainment period (CanAm’s write-up available here). Now I will try to clarify a factor behind some confusion in sustainment discussions: the fact that an EB-5 investment involves multiple layers and multiple timeframes, each subject to different terms and different USCIS requirements. This post defines the investment timeframes and applicable requirements for post-RIA EB-5 investors (people starting the EB-5 process after March 2022), and suggests questions for potential investors to ask about investment exit timing.

EB-5 Investment Flow Chart

A regional center investment involves at least two deals: one between the EB-5 investor and the new commercial enterprise (NCE) and one between the NCE and a job-creating entity (JCE) that deploys EB-5 capital in a project.

Typical EB-5 process steps (illustrated in the EB-5 Investment Flow Chart below)

EB-5 investor capital deposited in the NCE account

NCE uses EB-5 capital to fund a loan or make an equity investment in the JCE

The JCE spends capital in a project to cover project costs

The JCE repays loan or equity to the NCE (Optional: 4.1-4.2 The NCE reinvests EB-5 capital, if necessary for sustainment, and gets repaid)

EB-5 investor exit from the NCE

When discussing the EB-5 investment timeframe, often the investor assumes that we’re talking about the time from step 1 to step 5 – from the date he invests his money to the date he realizes a return. But when a regional center says “it’s a five-year deal,” this usually refers to the time from step 2 to step 4 – from the date the regional center issuer invests EB-5 capital to the date the issuer expects to be repaid. Meanwhile, when USCIS speaks of the 2+ year minimum “required investment timeframe” for sustainment, it is focused on the interval between step 3 and step 4 – starting from the date that an investor’s EB-5 capital is actually deployed in a project through the period that the capital remains deployed at risk.

Note: the “start date” for a USCIS-defined at-risk investment is later than the date of an investor’s deposit in the NCE account, while the investor’s repayment by the NCE is later than the NCE’s exit from a project. It might be only very little later, as when the NCE immediately transfers investor capital to the JCE, which immediately spends the money in a project, and the NCE goes on to repay the investor immediately after the JCE repays the NCE. However, Timeframe 1-to-5 could also end up years longer than Timeframe 2-to-4 or 3-to-4. If the project development process is lengthy or delayed, an individual investor’s funds might not be used until months or years after the date of the investment deposit. The deal between the EB-5 investor and NCE might have an exit significantly later than the NCE’s exit from its investment in the JCE, particularly in the past when immigration delay forced redeployment. With the large potential differences between investor, project, and USCIS timeframes for investment, it’s important to be clear about the different timeframes and to know which requirements and considerations apply to each.

Timeframe 1-to-5: Timeframe of the EB-5 investor’s investment in the NCE

The timeframe of the EB-5 investor’s investment in the NCE starts when an EB-5 investor deposits $800,000 or $1.05 million in the NCE and ends when the NCE repays/provides an exit the EB-5 investor according to the terms of the NCE offering.

The timeframe of the EB-5 investor-NCE deal CANNOT be guaranteed, per EB-5 rules. To quote precedent decision Matter of Izummi: “For the alien’s money truly to be at risk, the alien cannot enter into a partnership knowing that he already has a willing buyer in a certain number of years.” The USCIS Policy Manual at USCIS PM 6(G)2 explains that post-RIA capital does NOT count as invested capital if it is “subject to any agreement between the investor and the new commercial enterprise that provides the investor with a contractual right to repayment, such as a mandatory redemption at a certain time or upon the occurrence of a certain event, or a put or sell-back option held by the investor, even if such contractual right is contingent on the success of the new commercial enterprise, such as having sufficient available cash flow.” (See the Policy Manual for discussion of the limited redemption language allowable in the EB-5 investor-NCE agreement.)

USCIS rules give no ceiling to how long the NCE can hold EB-5 money, but they do define some minimums. USCIS rules for post-RIA investors specify that the EB-5 investor’s exit from the NCE can only be after job creation, after I-526 filing, and after the investment has been sustained “at risk” (i.e. deployed, not just in a bank account) for at least two years. For pre-RIA investors, the EB-5 investor exit must be at least after the investor has completed the two-year conditional permanent residence period.

One regional center offering has multiple investors, each with his or her own investment deposit date (which could be months or years apart). Therefore, a variety of individual investor timeframes will overlap the project timeframe and NCE-JCE deal timeframe in different ways. The NCE offering may or may not anticipate treating EB-5 investors as a group when deploying or repaying capital, despite the investors’ different start dates.

Timeframe 2-to-4: Timeframe of the NCE’s investment in the JCE

The timeframe of the NCE’s investment in the JCE starts when the NCE uses EB-5 capital to fund a loan or equity investment in the JCE and ends when the JCE repays/provides an exit to the NCE.

The duration of the NCE-JCE deal timeframe CAN be specified. USCIS rules allow the NCE-JCE deal to be a debt arrangement with a set term. Unlike the EB-5 investor-NCE agreement, the NCE-JCE agreement can have relatively firm redemption language. The EB-5 investor must look to the NCE’s investment horizon as reference for her own potential timeframe for exit.

The NCE’s investment in the JCE may be funded over time and can have a start date that pre-dates or post-dates the subscription of Investor X in the NCE. The prospective EB-5 investor should keep in mind that sales statements like “it’s a five-year deal” do not refer to directly to her prospective timeframe, but to the in-progress or future term of the deal between the NCE and JCE.

It can happen that a JCE repays the NCE early, before all EB-5 investors have finished their immigration-required minimum investment periods. In case of such timeframe mismatch, the solution is redeployment. EB-5 investors can still meet requirements so long as the NCE reinvests their funds in another project until the immigration-required sustainment period has been fulfilled (see USCIS PM 6(G)2).

It can happen that EB-5 investment reaches the JCE late, after the JCE has already finished spending money and creating jobs. Bridge financing provides a limited solution for project-investor timeframe mismatch. An EB-5 investor can potentially claim credit for contributing to a completed project and job creation, provided her investment is replacing qualifying bridge financing (see USCIS PM 6(G)2), and USCIS training materials on bridge financing). However, the most straightforward case for EB-5 credit is based on sequential timeline: EB-5 capital enters the JCE followed by job-creating activity.

For post-RIA investors, the USCIS-required sustainment timeframe starts when the investor’s full $800,000 or $1.05 million is “placed at risk” and ends a minimum of two years later.

To quote the USCIS Q&A on “Required Investment Timeframe” for post-RIA investors: “INA 203(b)(5)(A)(i) states that, to be eligible for classification, the investment must be ‘expected to remain invested for not less than 2 years’” and “For purposes of determining the date when the two-year period required by INA 203(b)(5)(A)(i) begins, we will generally use the date that the requisite amount of qualifying investment is made to the new commercial enterprise and placed at risk under applicable requirements, including being made available to the job creating entity, as appropriate.”

“Placed at risk” is a defined term in EB-5. An investment counts as “at risk” once these conditions have been satisfied: the full amount of investment is made available to the job-creating entity (not just sitting in a bank account, but in use), the JCE has business activity, and the investor has a risk of loss and chance for gain with no guaranteed return (see USCIS PM 6(G)2). For examples of cases where EB-5 investor funds were deposited in the NCE, but did not count as “at risk” because not fully deployed to the JCE, see the precedent decisions Matter of Izummiand Matter of Hoand non-precedent decisions such as APR052018_05B7203, APR022018_01K1610, JAN222021_04B7203, MAR032021_01B7203, and FEB242022_01B7203.

The start date for “at risk investment” could be interpreted as the date that the investor’s full $800,000 or $1.05 million is transferred from the NCE account to the JCE account. More conservatively, it could be interpreted as the date on which the JCE finishes spending EB-5 investor money, since that’s the date by which the investment has unambiguously been fully “made available to the job creating entity.”

As discussed above, the USCIS-required sustainment timeframe has a start date equal to or later than the date of the NCE’s investment in the JCE, which in turn is more or less later than the date of the EB-5 investor’s investment in the NCE. The investor ideally wants to seek an offering with an NCE-JCE deal slated to end comfortably more than two years later than the latest date the her invested capital could be deployed in the JCE. If the JCE repays the NCE earlier, then the investor will have to see her funds redeployed by the NCE in order to meet the 2+ year requirement. If the JCE repays later than the USCIS-required minimum investment period, there are no immigration consequences for the investor.

Conclusion: Questions for Prospective EB-5 Investors to Ask

When will the job-creating project start and finish spending EB-5 money?

Why to ask: The USCIS-required investment timeframe is indexed to when EB-5 money is deployed at risk, not just when it’s sitting in a bank account. The start date for the minimum two-year sustainment period is not the date of EB-5 investment, but the date that EB-5 money is made fully available to the job-creating entity.

Where to look for the answer: business plan schedule and budget.

When will my investment be released from the NCE to the JCE? What triggers the release?

Why to ask: The start date for the minimum two-year sustainment period is not the date of EB-5 investment, but the date that EB-5 money is made fully available to the job-creating entity.

Where to look for the answer: PPM and any fund administration documents.

Will the NCE release my funds to the JCE before the JCE finishes project expenditures and before the JCE creates jobs? If not, is there a good story for why my investment should get credit for funding job-creating activity?

Why to ask: To qualify, EB-5 investment must form a nexus with job creation. If investor money comes in after a project is already complete, then the investor faces additional hurdles to argue that the funds are still “at risk” and made available for job creation.

Where to look for the answer: Consult the business plan schedule and PPM to determine if your investment can come in before the project is completed and jobs are created. If not, have your lawyer scrutinize bridge financing documentation to ensure that the investment can still comply with EB-5 rules.

When will the project be economically able to support a capital event (e.g. loan refinance or profitable sale).

Why to ask: EB-5 investment is a real investment, and the planned exit strategy is only as good as the economics behind it. A three-year loan term between NCE and JCE is plausible only if the project is likely to be positioned in three years to allow refinancing or paying off the loan. If investor repayment depends on selling the project, then timing practically depends on when project value could plausibly support a profitable sale. Different types of projects require different holding periods; for example the average years-to-exit for a large-scale real estate development is naturally longer than for the average energy project. Industry averages and common sense can help apply a reality check to issuer promises, and help investors to consider the investment horizon that’s reasonable and to-be-expected for the type of project they want to invest in. If a deal promises an exit at a certain date regardless of project economics, be suspicious of whether this is a real investment or a reliable promise.

Where to look for the answer: business plan schedule, financial projections, market analysis, appraisal report, and Google.

What position does EB-5 have in the project capital stack?

Why to ask: EB-5 is generally just one of several sources in a project capital stack. Each source has a different position and priority when it comes to repayment. The likelihood of exit sooner rather than later for the NCE’s investment depends in part on the NCE’s level of seniority in the JCE capital stack.

Where to look for the answer: business plan and PPM.

Is my exit from the NCE contingent on any milestones in my immigration process (e.g. only after receiving a visa, only after I-829 filing, etc.)?

Why to ask: In the past, EB-5 offerings conditioned investor exit on completing the conditional permanent residence period, based on sustainment rules for pre-RIA investors. But USCIS does NOT require sustainment through the CPR period for post-RIA investors. Investors today need not accept an offering that still explicitly links investment exit timing to the risk of immigration process delay. According to USCIS, the sustainment requirement for post-RIA investors is linked to project milestones (using the capital, creating jobs), not to immigration milestones.

Where to look for the answer: PPM or other document describing the terms of the deal between investor and NCE.

Is my exit from the NCE contingent on the exit timing of other NCE investors?

Why to ask: You are looking for assurance that your exit timing won’t be delayed by another EB-5 investor with a much later timeframe than yours. That assurance could come if the offering allows for individual exits and/or if the span of individual investor timeframes is not large.

Where to look for the answer: PPM or other document describing the terms of the deal between investor and NCE.

Is the timing of my exit from the NCE guaranteed?

Why to ask: If the timing of EB-5 investor exit from the NCE is guaranteed in advance, then the investment likely does not qualify as “at risk” according to USCIS requirements, and USCIS will deny the case.

Where to look for the answer: If there is an I-956F approval, then USCIS should already have judged the offering redemption language to be acceptable. Otherwise, ask your EB-5-experienced immigration lawyer to review the documents to ensure that the terms of the deal between investor and NCE comply with requirements.