This post checks in with the backlog of EB-5 applicants with priority dates before March 15, 2022 who are still waiting for Unreserved visas.

The pre-RIA EB-5 backlog is spread across several locations. The following list notes the places where applicants may be waiting, and available information on inventory and progress for each location.

I-526 still pending

1,105 pre-RIA I-526 remained pending as of September 2025. These people mostly have old priority dates (the FY26 Q1 median processing time was 78.5 months) and many will likely be denied in the end. (The FY26 Q1 legacy I-526 denial rate was 49%, with just under 200 petitions processed.) This pool likely represents few future visa applicants.

I-526 approved but no I-485 or visa application filed yet

This number is unreported, but should be small and mainly limited to China-born applicants waiting for Chart B. (One might guess the number by comparing I-485 and NVC applicants with expected numbers given I-526 receipts and approvals and visas issued, but I haven’t tried.)

I-526 approved and I-485 pending for adjustment of status

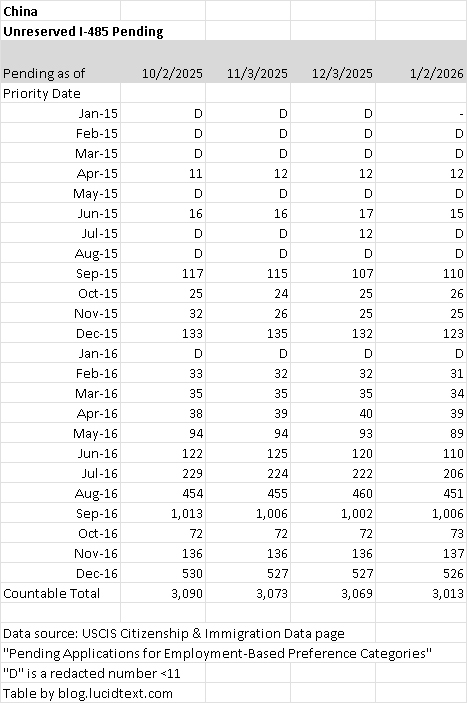

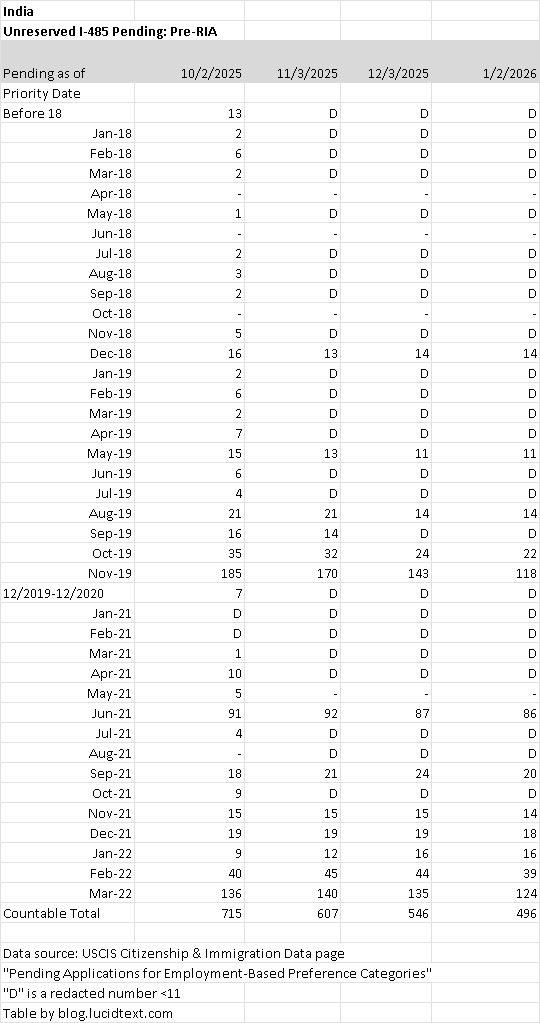

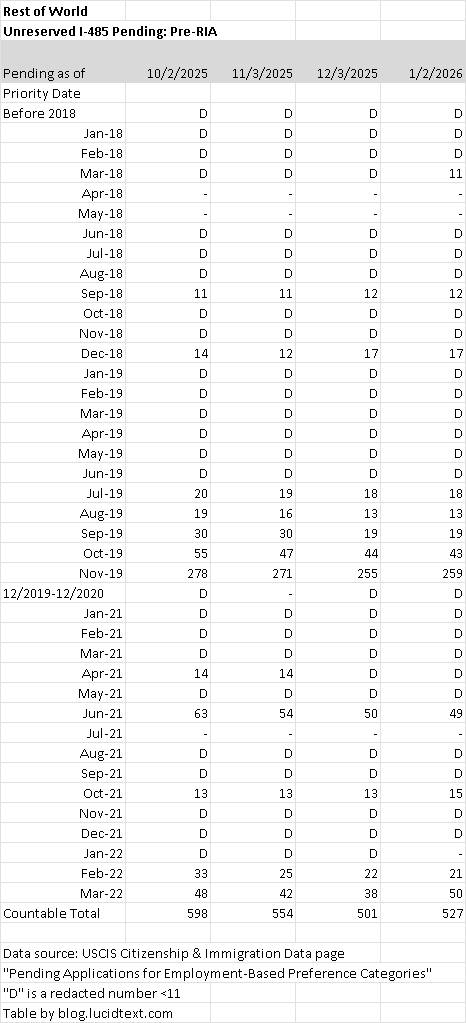

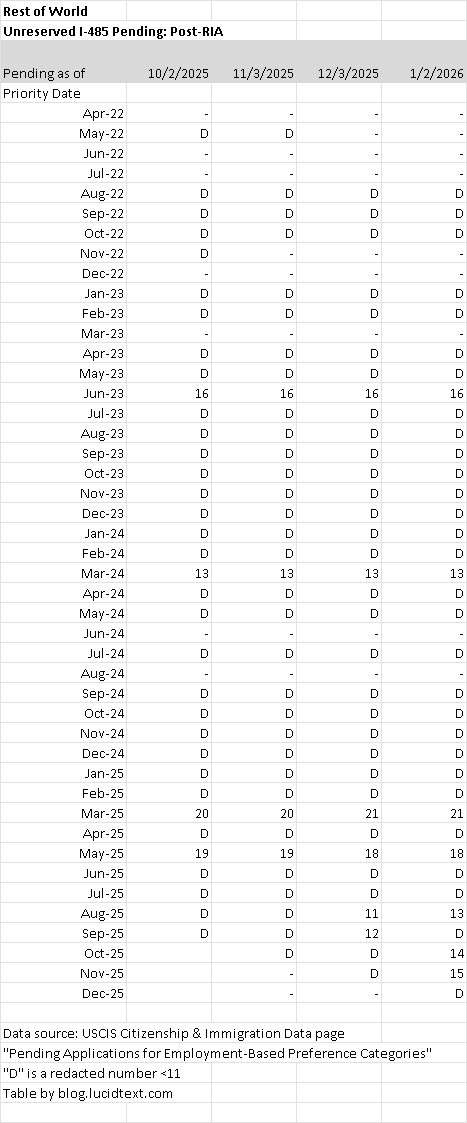

For pre-RIA, this pool should be just a bit smaller than the total pending I-485 inventory, for which we now have data through January 2026. See below for detailed inventory charts. As of January 2026, the pending pre-RIA Unreserved I-485 inventory was roughly 4,000, including around 3,000 from China, 500 from India, and 600 from Rest of Word. The inventory grows as the Visa Bulletin moves China Chart B and more I-485 get filed, and shrinks as visas get issued. It appears that in FY2026 Q1, AOS Unreserved visa issuance may have been around 100 to China, 220 or so to India, and 75-150 to Rest World.

I-526 approved and registered with the National Visa Center, waiting for consular processing

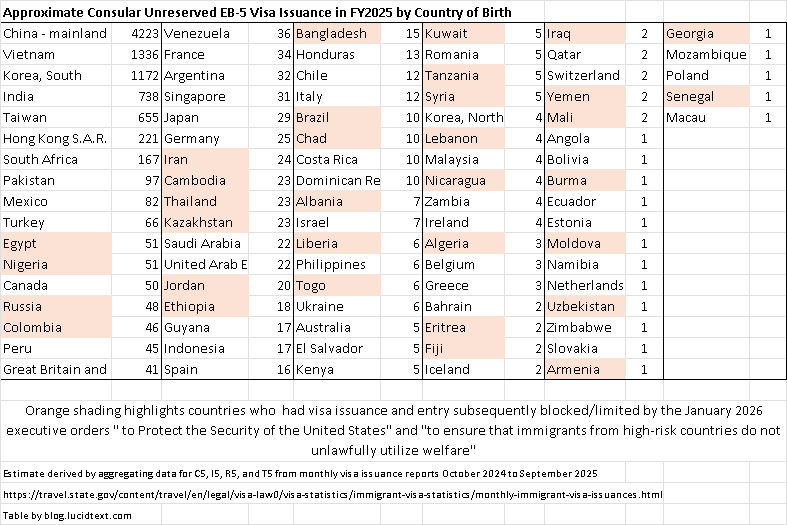

Department of State used to regularly report on the NVC inventory, but has not updated the official NVC waitlist report since 2023. The last available data is thanks to an IIUSA conference presentation in May 2024. As of May 2024, the NVC waitlist recorded 31,255 pending EB-5 applicants from China, 2,541 from India, and 5,774 from Rest of World. We can guess how many remain today by looking at I-526 approvals and consular visa issuance since May 2024, and guessing how the NVC inventory has been increased since 2024 by petition approvals and decreased by visa issuance, denials, giving up, etc. I guess that the NVC waitlist now has more than 20,000 but fewer than 28,000 pre-RIA applicants still waiting. See below for available detail on EB-5 Unreserved visa issuance in FY2025.

The data file linked to my EB-5 Timing page collects pre-RIA data on the Pre-RIA Data tab, and sets up a current backlog estimate by country on the Unreserved tab. Feel free to work with the data and add your own assumptions.

EB-5 Unreserved I-485 Inventory Detail

The following tables summarize the latest information about the pre-RIA Unreserved I-485 inventory in the reports “Pending Applications for Employment-Based Preference Categories” just published by USCIS for October 2025 to January 2026. One can get a rough sense of I-485 processing activity by looking at inventory differences month-to-month.

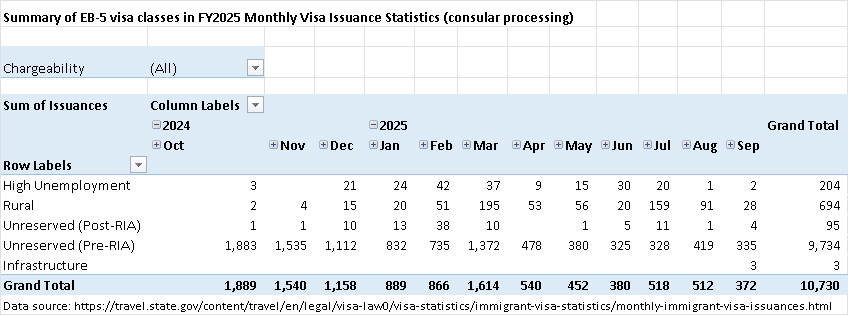

FY2025 Consular Visa Issuance

Official and exact FY2025 visa issuance numbers will not be available until Department of State publishes the next annual report. But I made a preliminary rough estimate by summing monthly reports for EB-5 Unreserved visa issuance from October 2024 to September 2025. I used yellow shading to highlight countries who are now blocked/limited by January 2026 executive orders from visas and entry. Sorry $800,000 investor in our economy — you can’t come into our country because you’re congenitally likely to use welfare [face palm]. But congrats to everyone who managed to get EB-5 visas before the 2026 orders, including 10 from Chad, my happy childhood home.

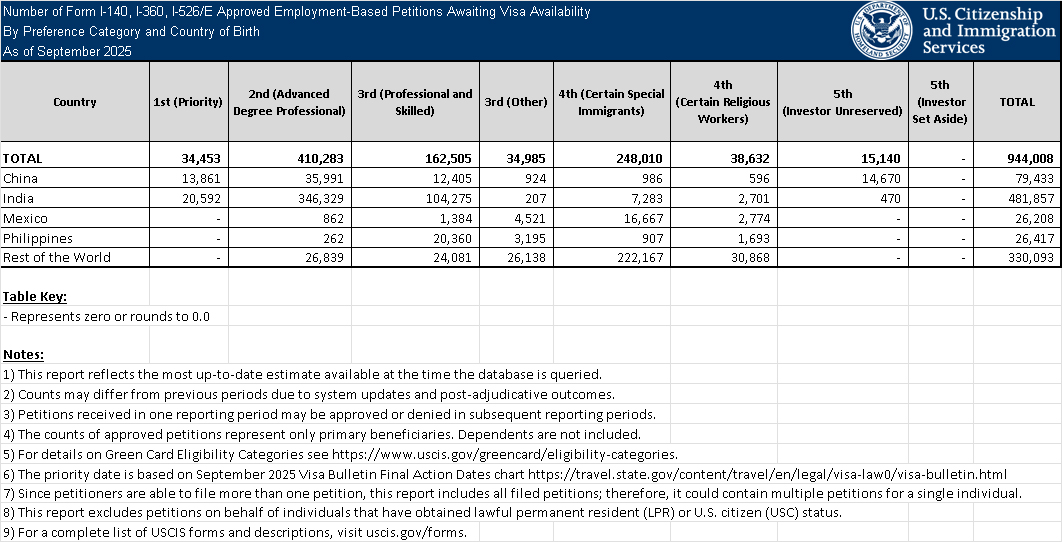

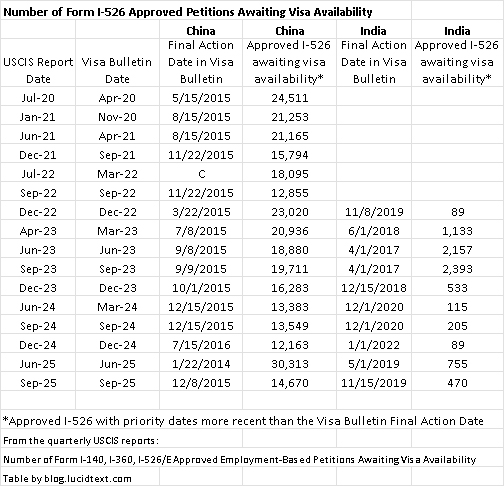

This report looks as if it gives useful information about the EB-5 visa backlog, but it does not. It gives a very specific data point: the number of I-526 petitions that USCIS has approved, as of the report date, that have priority dates later than the Final Action Date in the concurrent Visa Bulletin.

This data point would be meaningful if the Visa Bulletin never retrogressed, and one could assume that everyone with an I-526 approval later than today’s Visa Bulletin’s Final Action Date has no visa yet. But that assumption does not hold in EB-5, given the final action date swings for China and India in recent years. So the USCIS report does not show the backlog of people still waiting for EB-5 visas, or reflect progress in issuing visas. The table below puts the most recent September 2025 USCIS report in context of the referenced Visa Bulletins and past USCIS reports.

For example, the number of “approved I-526 awaiting visa availability” for China plummeted from over 30,000 in the June 2025 USCIS report to under 15,000 in the September 2025 report. That difference tells us nothing about visa issuance or processing activity between June and September 2025. The different Visa Bulletin dates in June and September caused USCIS to be counting a different segment of I-526 approvals for each report. We can conclude from the report comparison that about 15,000 approved China I-526 have priority dates between January 2014 and December 2015. That’s about all we can conclude. The USCIS report cannot mean that these principals mostly don’t have visas yet, since Department of State has been issuing visas past January 2014 for years already per past Visa Bulletins. The report also cannot mean that these principals just received visas, since 15,000 visas cannot have been issued to China between June and September 2025.

Looking at the India column, I compare the USCIS reports from December 2022 and September 2025 — a relatively apples to apples comparison because the Visa Bulletin had a Final Action Date in November 2019 for India in each of these months. The comparison tells me that USCIS had processed more of its post-2019 I-526 inventory by 2025 than it had as of 2022. I cannot conclude that most or all of the 470 Indian investors who had gotten I-526 approval by September 2025, according to the USCIS report, did not also have a visa already by September 2025.

Note

Is this analysis helpful for you? Please consider making a contribution to support all the work that goes into it. I have set up Paypal and Stripe links, and can also offer individual consulting.

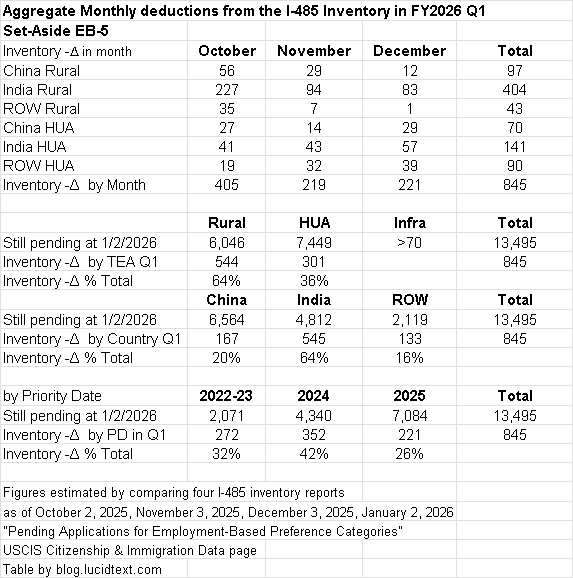

I take each month’s inventory report and compare it against the previous month, to get a sense of visa activity. For example, the inventory of China Rural I-485 with December 2022 priority dates shows 61 pending forms as of October 2, 2025, down to 53 on November 3rd, 51 on December 3rd, and 50 on January 2nd. I look at those numbers and guess that 11 Rural visas may have been issued in FY2026 Q1 to China-born Rural applicants with December 2022 priority dates.

If net deductions from the I-485 inventory roughly represent visas issued, then over 800 set-aside EB-5 visas were issued through status adjustment in the first three months of FY2026. That’s twice the average quarterly AOS volume for set-asides in FY2025 — a good sign so far as it goes. If FY2026 set-aside visa issuance overall can double last year’s volume, then all available set-aside visas can be used this year. I note, however, that I-485 movement started strong in October and then tapered off in November and December. We shall see what happens next.

As usual, I-485 inventory deductions were spread over a wide range of priority dates — a reminder that the process is not exactly FIFO by priority date. Activity continued to be particularly concentrated in the Rural category, and on India-born applicants. I note that the I-485 inventory does capture some pending Infrastructure applicants, but with numbers small enough to be redacted with the letter “D”. The following table highlights interesting stories in the I-485 data.

Consular Processing Update

Department of State has posted the Monthly Immigrant Visa Issuance report for September 2025, completing FY2025. I am disappointed to see no year-end surge in consular Unreserved visa issuance (which I’d thought might happen considering the year-end Visa Bulletin notes and date movement for China), but excited to see Infrastructure visas finally making the scoreboard.

Note

Is this analysis helpful for you? Please consider making a contribution to support all the work that goes into it. I have set up Paypal and Stripe links, and can also offer individual consulting.

Thank you again to USCIS for publishing a dedicated EB-5 report with country-specific and category-specific I-526/I-526E data. This detail is so important for backlog and wait time analysis, and now we don’t have to sue to get it.

The major news: EB-5 demand dropped overall in Q4 (particularly from China and India), and processing volume remained low overall. That means that the set-aside backlog growth rate slowed in Q4, and the near-term risk of Visa Bulletin retrogression did not increase very much. Meanwhile, approval rates remained generally high.

As usual, I copied the quarterly data into my spreadsheets and made a variety of charts that put the data update in context of wider trends.

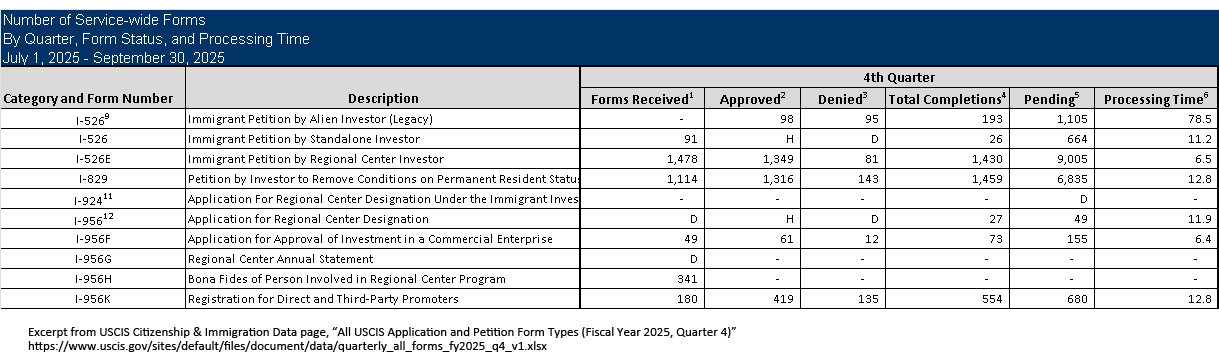

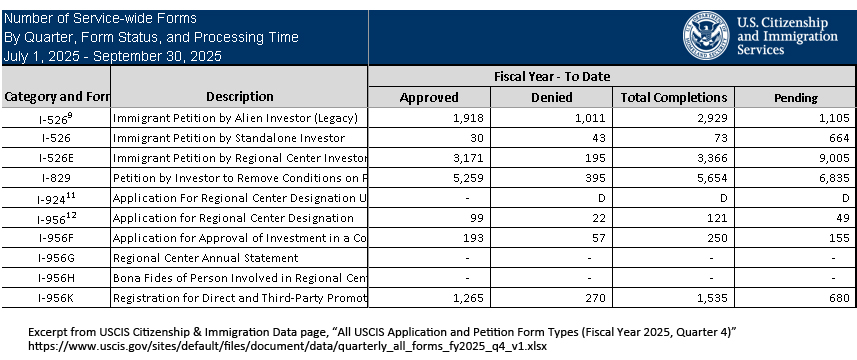

All Forms Report Summary

For convenience, I made image excerpts of EB-5 data in the “All Form Types” report. Note that the Q4 table includes a column for median processing time in months for each form. The Fiscal Year table provides a nice summary of all EB-5 activity in FY2025.

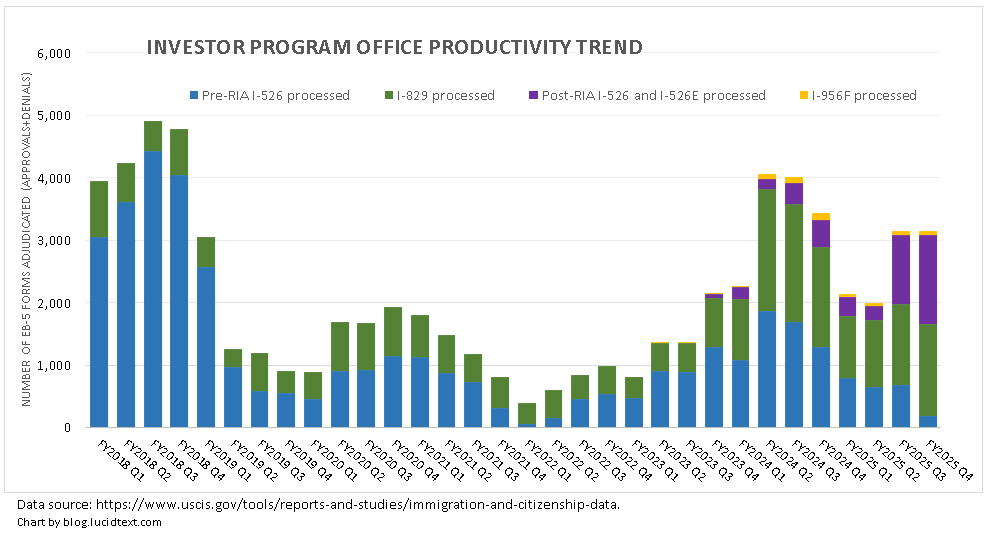

IPO Productivity Trend

Overall, IPO processed about the same number of forms in Q4 as in Q3. A drop in the number of legacy I-526 processed was counterbalanced by a few hundred more I-526E and I-829 completions. But in context of past performance, IPO productivity still looks quite low.

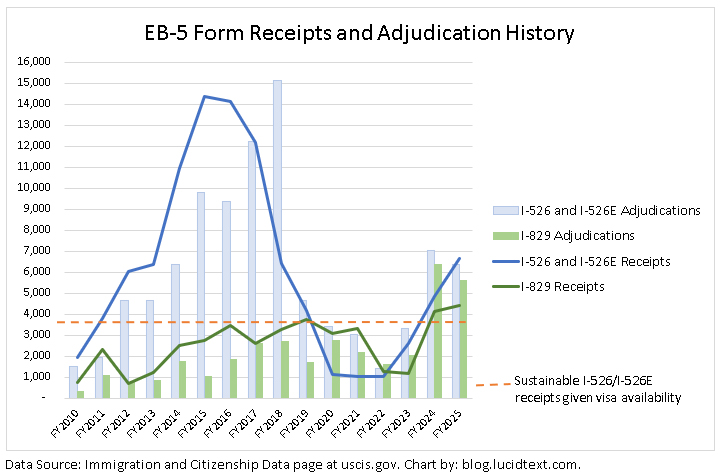

Receipt and Processing Volume Trend

FY2025 ended with more investor petitions filed but fewer investor petitions processed than in the previous year. The following chart compares annual receipt numbers against (1) annual processing volume, and (2) the average number investors who can be accommodated in a year of visas. In years when receipts exceed processing volume, then pending petition backlogs grow. In years when receipts exceed annual investor visa numbers, then visa backlogs grow. FY2025 slightly shrank the pending petition backlog at USCIS, but grew the pipeline backlog of applicants seeking future visas.

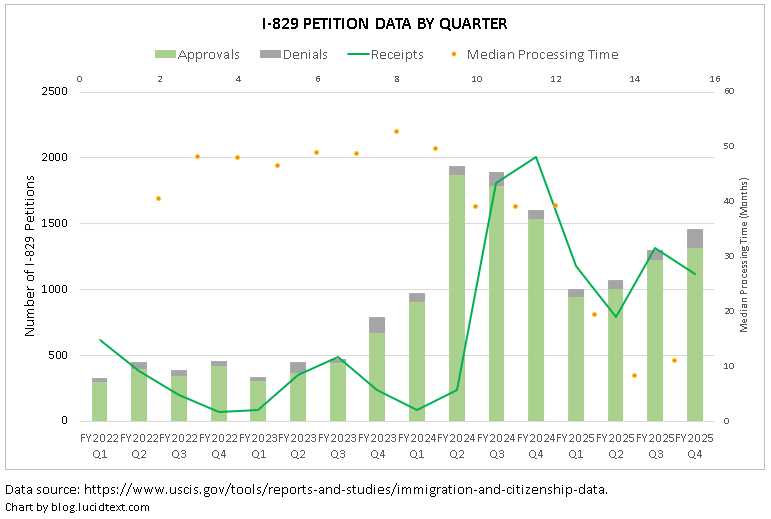

I-829 Processing Trend

USCIS processed a few more I-829 in Q4 than in the previous quarter. The approval rate was 90% — a bit lower than previous quarters – and the median processing time inched up to 12.8 months.

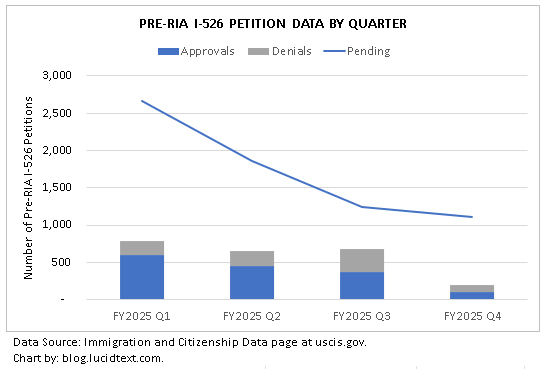

Pre-RIA I-526 Processing Trend

A few legacy I-526 remain pending, but USCIS dramatically cut legacy I-526 processing activity in Q4. These unfortunate old petitions, previously held up by the Visa Availability Approach to China I-526 processing, are getting a lot of denials now (49% denial rate in Q4).

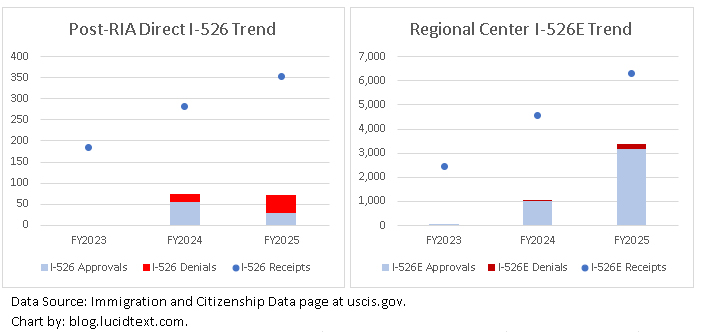

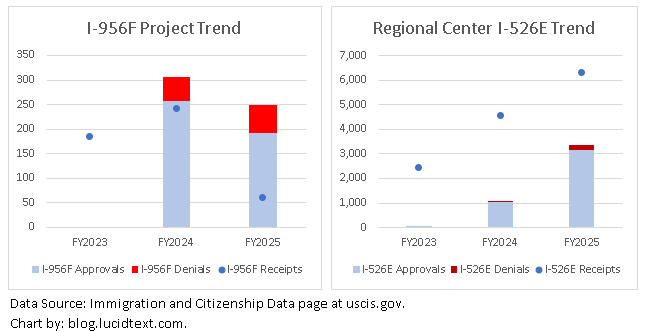

Post-RIA I-526, I-526E, and I-956F Processing Trend

I-526E processing picked up a bit in FY2025, but not nearly enough to close the distance with receipts. Denial rates remained low for regional center I-526E and high for direct EB-5.

USCIS has been processing a good volume of I-956F – more than enough to keep up with receipts and prevent a pending backlog. I note that I-956F project denials have increased slightly, which will eventually result in denials for I-526E associated with those projects.

Post-RIA Demand Trend

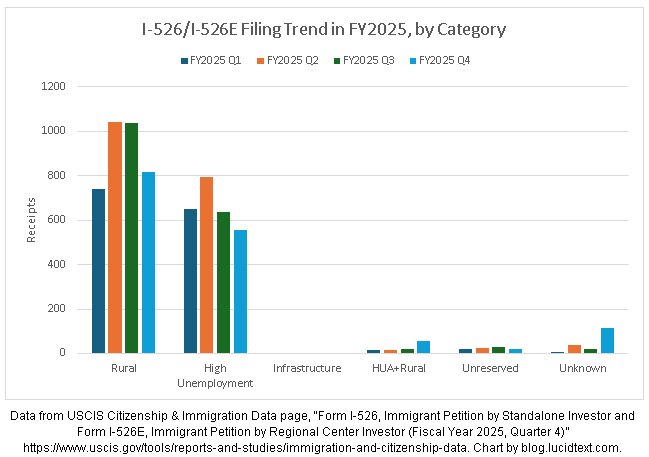

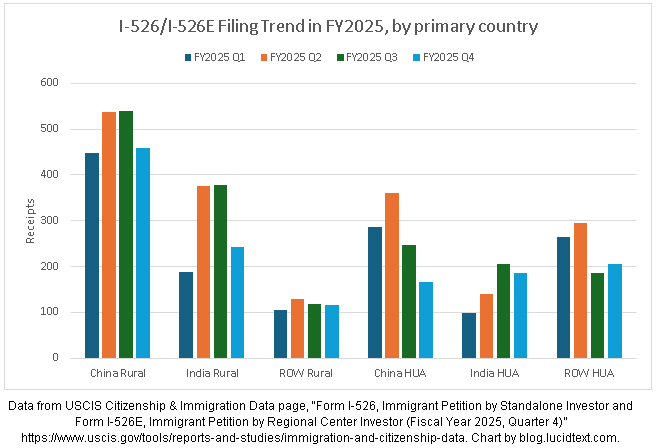

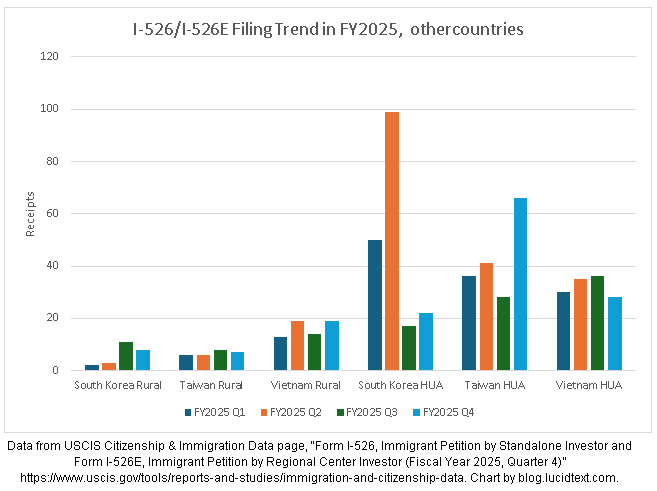

The report of I-526/I-526E receipts by country and TEA category shows some shifts in Q4 as compared with Q1-Q3. I-526/I-526E receipts dropped for both Rural and High Unemployment in Q4, and from both China and India. “Rest of World” demand picked up in Q4. I don’t know if this will prove a trend, but it would make sense as a self-regulating response to education about backlogs. I have wondered about a potential demand surge as the grandfathering deadline approaches, but no such surge had started as of July to September 2025, at least. The Q4 report continues to report “0” for Infrastructure I-526E filings in every month, though we know that Infrastructure I-526E were filed before September 2025. (For example…)

Note

Is this analysis helpful for you? Please consider making a contribution to support all the work that goes into it. I have set up Paypal and Stripe links, and can also offer individual consulting.

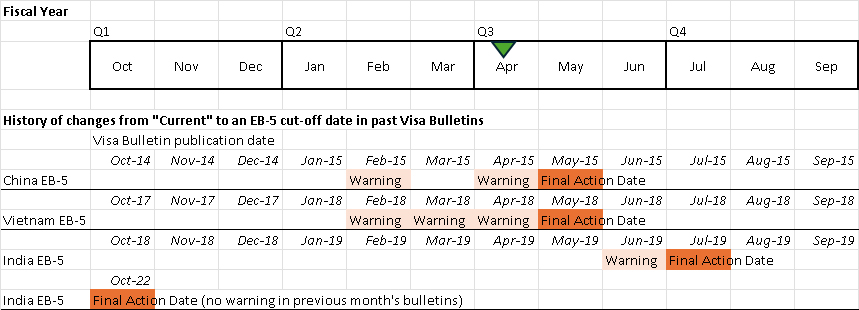

April starts the third quarter of the fiscal year – a prime time for Department of State to reassess progress with annual visa issuance and cut-off dates. I anxiously awaited the April 2026 Visa Bulletin, wondering whether we’d finally see a warning note for EB-5 along the lines of “It may become necessary to establish Dates for Filing and Final Action Dates to ensure that issuances in set aside categories do not exceed annual limits.” But, the April bulletin has no such note.

Looking back, the first-time EB-5 final action dates for China and Vietnam both came in a May Visa Bulletin, and were preceded by several months of warning notes. India got its first-ever EB-5 cut-off date in a July Visa Bulletin, with one warning in the previous month. (India EB-5’s second change from “Current” to a final action date came in the first Visa Bulletin of fiscal year 2023, with no prior warning.)

Considering the history, the continuing Visa Bulletin silence on set-asides — even to April 2026 — makes me guess that Department of State is not making good progress in issuing the 6,400 or so set-aside visas available in FY2026. (I look forward to hearing Charlie’s take on this next week, and appreciate WR Immigration continuing to post cautions about how to interpret/misinterpret the Visa Bulletin and AOS window.)

The April 2026 Visa Bulletin does repeat the general note that “Immigrant visa issuance rates for aliens from certain countries have decreased in light of various actions the administration has taken” and therefore “dates for filing and final action dates have been advanced across various immigrant visa categories” [allowing more visa issuance to those select aliens and countries not blocked by many administrative actions]. China Unreserved advanced from August 15, 2016 to September 1, 2016. The movement is small but could result in visas for quite a few applicants, considering that 5,334 Chinese investors filed I-526 between July 2016 and September 2016 (per IIUSA FOIA Request COW2017000616).

Just a note that I made a significant revision to the 2026 Backlog post published yesterday. (And to the corresponding Summary2 and Infra tabs in the Excel linked to my EB5 Timing page.) The calculation now reflects the monthly visa issuance data just published and — more significantly — more Infrastructure demand. A kind reader brought to my attention a couple large Infrastructure projects not previously on my list. Adding hundreds more Infrastructure investor slots to the log, plus a recent flurry of approvals, required striking most of my backlog analysis for Infrastructure. If only we had timely data from the government for reference, instead of having to piece together anecdotes! And once again, I’m impressed with the thought of how desperately EB-5 needs and deserves more visa numbers to support its demonstrated economic potential. The supply we’re working with is just too small, when one good project can overflow years worth of visas.

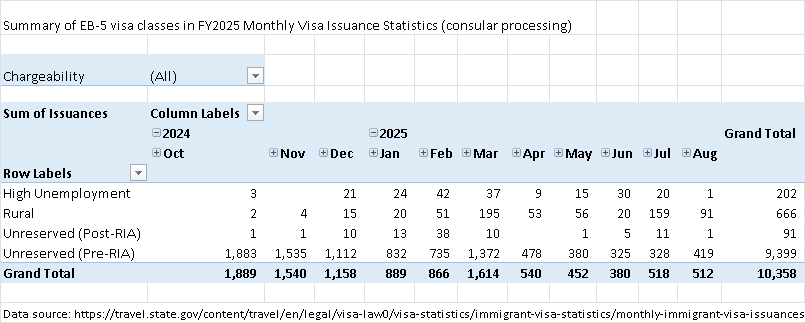

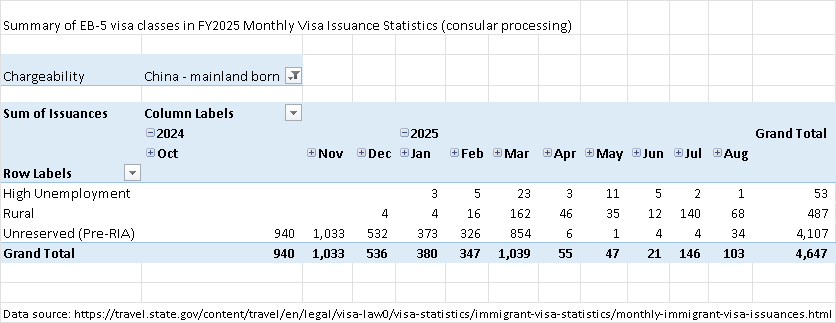

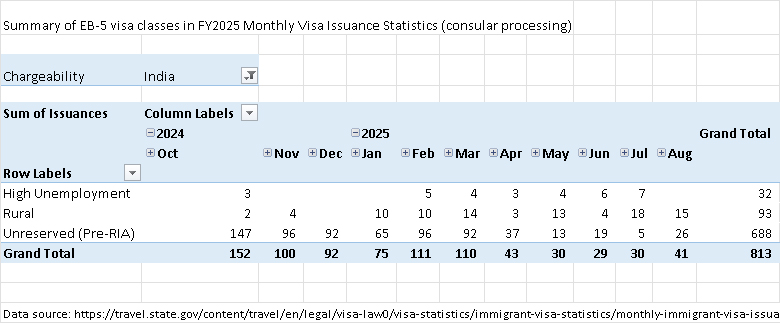

I shall claim credit! Hours after I finally gave up on government updates and published my important 2026 backlog post without new data, Department of State updated the Monthly Visa Issuance Statistics page for the first time in nine months. Now we know for sure how many EB-5 visas were issued through consulates in June, July, and August 2025. The numbers are about what I’d guessed — a bit higher for Rural and lower for High Unemployment, and higher for India and lower for China than I’d expected. But it’s really great to see solid numbers again, thank you DOS! Now we just need the NVC waitlist and FY2026 visa limit. The following pivot tables summarize FY2025 monthly consular visa issuance, now including June to August.

[3/6 UPDATE: I have updated the tables and Infrastructure discussion in this post after Department of State published some additional visa issuance data, and I became aware of two additional Infrastructure projects.]

Where are we with EB-5 visa backlogs and wait times as of early 2026?

I have been holding off on this article, thinking that USCIS and/or Department of State would publish more data any day. But the government has maintained its silence since May 2025 as to visa issuance, and silence since June 2025 about the progress of petition receipts and adjudications. But still, we can’t afford to just keep looking at old numbers and thinking as if it were still 2025. The ground has shifted.

This article reviews developments that appear particularly significant to me:

Set-aside backlog growth since last I-526E report

Significance of Unreserved visa availability and access

Infrastructure category activity and outlook

Processing sequence factors and changes

Visa bulletin outlook compared to backlog outlook

Set-Aside Backlog Growth

EB-5 backlog numbers, whatever they may be exactly, are certainly not the same as they were as of mid 2025. Industry chatter suggests undiminished incoming set-aside investor demand, even as the silent Visa Bulletin suggests on-going low set-aside visa issuance.

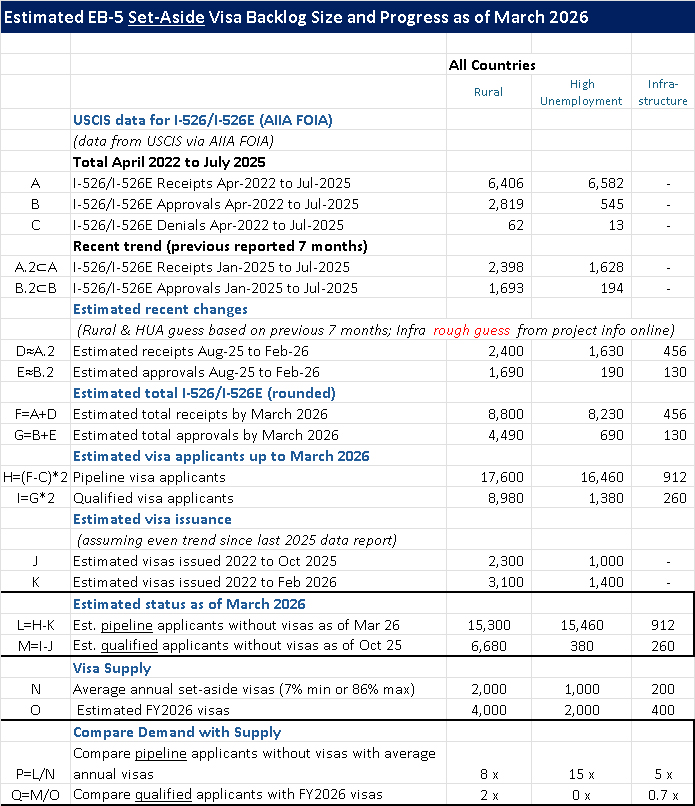

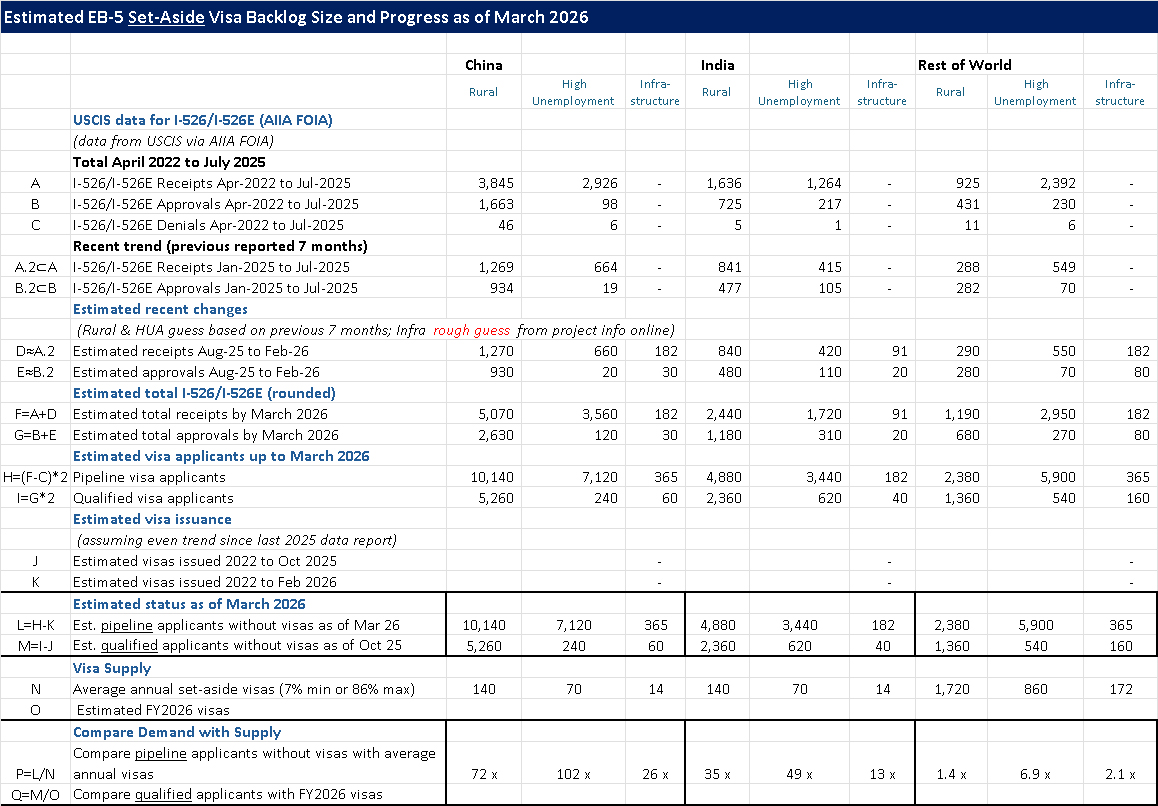

For a tangible reference in absence of recent EB-5 data, I made a napkin calculation. I took the FOIA numbers we have for I-526/I-526E receipts and approvals through July 2025, and advanced them to the present day with a simple assumption: what if the past seven unreported months mirrored the previous seven reported months. (This calculation is spelled out in the “Summary2” tab now added to my EB5 Backlog Analysis file linked on the EB5 Timing page, and also represented in image thumbnails below. With thanks again to AIIA and Alexandra George of Galati Law for getting data through FOIA as of January 2025 and July 2025, to Google and industry colleagues for Infrastructure intel, and to the government for publishing at least some data in 2025.)

The take-away: if the EB-5 train kept going at its previous reported rate, then by now over 30,000 people are in process heading toward set-aside visas, including over 15,000 each in Rural and High Unemployment, and potentially around 1,000 in Infrastructure. (I call these people “pipeline applicants,” meaning I-526/I-526E filed and investors plus family in the pipeline to claim visas eventually — though most don’t qualify for a visa yet since they are still waiting for the investor petition approval. For the sake of estimate, I make my typical assumption of average two future visa applicants per I-526/I-526E filed, after denials and with family, though the reality could turn out higher or lower than that.) Think about the wait times, if 30,000+ people are in queues headed for windows with just over 3,000 visas to give in a typical year.

Drilling down by country emphasizes set-aside retrogression risk for new investors as of March 2026. If every applicant in the high unemployment area pipeline had to take a high unemployment area visa, then even the new “rest of world” investor (not from China or India) would face a 6+ year HUA visa wait time and Visa Bulletin retrogression, while China-born and India-born investors would theoretically face multi-decade HUA visa wait times. That’s based on looking at the bottom line of the backlog table above — at the difference between pipeline applicants as compared with annual category visas: 6.9x excess for “rest of the world” in high unemployment (even if ROW gets all HUA visas above country caps) and a shocking 49x excess for India and 102x for China. Those massive HUA pileup estimates reflect what would happen if every high unemployment investor and family had to take a high unemployment visa, and if Rest of World demand continued as it has been. The calculation within Rural is less dire than for HUA, considering the double set-aside portion plus less excess demand from Rest of World. But the Rural inventory numbers are still high enough (and the supply numbers low enough) to add up to multi-decade wait times for China and India — if every Rural investor has to take a Rural visa. (But that shouldn’t be so, as further discussed below…)

Meanwhile, the Unreserved backlog has been shrinking. Pre-2022 investors from China and India have apparently been getting a good volume of visas, the Visa Bulletin is advancing dates, and few new investors are heading exclusively for Unreserved by making $1.05M investments.

The upshot: the backlog picture has flipped. When RIA passed in 2022, Chinese and Indian investors faced prohibitive legacy backlogs in Unreserved but clear lanes ahead toward Rural, High Unemployment and Infrastructure visas. For new investors in 2026, the greatest imbalance appears to be on the set-aside side.

Unreserved Visa Availability and Outlook

Once set-aside lanes are unquestionably overcrowded, the hope for a visa number has to depend on Unreserved visas being also on the table for today’s set-aside investors. We are to the point where, effectively, many new set-aside investors are not investing for set-aside visas. Incoming investors from China and India, in particular, are not counting on multi-decade waits for the corresponding set-aside visa. They are relying on the chance to also access Unreserved visas in priority date order, regardless of which type of investment they choose.

Concluding that today’s EB-5 visa wait times depend so heavily Unreserved visas, I have been sweating over the question of Unreserved visa access for set-aside investors.

On the positive side, the theory looks solid. I-526E approval notices for set-aside investors continue to list “Unreserved” as well as “Reserved” as “approved visa classifications.” Department of State published a process for consular applicants to request a visa category from among the options on the approval notice. Immigration lawyers mostly seem optimistic. (For example, listen to 11:30-22:11 in this February 2026 webinar for Carolyn Lee’s thoughtful response to my grilling on Unreserved visa access.)

On the positive side, the Unreserved category made a huge leap forward for India in the January 2026 Visa Bulletin, and may be about to advance quickly for China as well. (The March 2026 Visa Bulletin notes a windfall of extra visas headed for the countries not blocked by President Trump’s various visa orders). Until recently, I had been looking at 2024 data and typical allocations, and thinking that the pre-2022 Unreserved backlogs wouldn’t be out of the way until 2030 for India and the mid/late 2030s for China. Now it looks as if pre-2022 EB-5 priority dates might all be cleared from waiting lines by 2027 for India, and maybe even before 2030 for China. And then there would be opportunity for backlogged post-RIA set-aside investors from China and India to overflow into the larger Unreserved pool.

On the worrisome side, there isn’t friction-free access to Unreserved visas for set-aside investors. USCIS has not yet followed Department of State in establishing a process whereby an I-485 applicant can pro-actively request an Unreserved visa. It naturally hasn’t been a priority for USCIS in this period when set-aside visa supply has gone under-used anyway, but I’ll feel better when I see a process. I also worry about whether the new I-526E inventory management approach just announced by USCIS could limit I-526E adjudication according to set-aside visa availability, erecting another speedbump to Unreserved visa usage.

On the worrisome side, I watched and raged at what happened leading up to 2022, when a new law took 3,200 previously unreserved EB-5 visas and set them aside in new categories untouchable by the legacy backlogged applicants who had been counting on access to those numbers. (Reminded now of what I got right and wrong in old posts on this.) As TEA backlogs have now grown anew, could lobbyists today be dreaming of another carve-out to circumvent backlogs and reduce future unreserved visa availability to today’s investors? They had better not be, but I wish I knew for sure that this couldn’t happen. Prospective investors today must be able to rely on priority date/country-specific access to the full pool of Unreserved visas, or else they will stop considering Rural, High Unemployment, or Infrastructure investments in light of backlogs.

Potential Unreserved Visa Impact

What’s the best possible outcome, assuming no limits or friction to future Unreserved visa access for today’s set-aside investors? How good can visa wait times look, if we can assume that everyone already in process gets efficiently matched with the first qualifying category visa available, including Unreserved, according to priority date and country-specific priority?

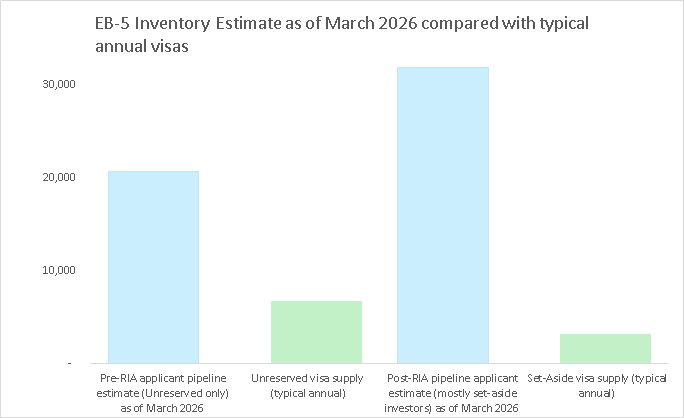

As discussed above, the existing EB-5 pipeline to be accommodated by now appears to include about 20,000 old applicants who can only take Unreserved visas, plus 30,000+ applicants with more recent priority dates who could take their set-aside or an Unreserved visa. (The tables above show the numbers by country, and my linked spreadsheet shows the data, assumptions, and calculations behind the rough estimate.)

It would take five full normal EB-5 visa years to issue visas to 50,000 pipeline applicants if country and category limits didn’t apply, or if incoming EB-5 demand shortly stopped for good. When one tries grappling with country-specific and category-specific factors, and assuming on-going demand from Rest of World countries, the calculation can only get worse than the baseline for China and India, while looking better for Rest of World.

I made myself some big spreadsheets to work with the sorting question, experimenting with how the pipelines of Pre-RIA, Rural, High Unemployment and Infrastructure investors from China, India, and Rest of World might get optimally matched into available EB-5 visa pools (and react to a variety of scenarios on factors like family sizes and denial rates and ongoing demand). I can make my spreadsheet conclude that Chinese and Indian investors with priority dates through 2026 could all have been matched with visas by 2033 or so, regardless of the TEA category in which they invested. I’m not putting the spreadsheet on the Internet because it’s a low-confidence conclusion, with many assumptions and elaborate setup that take a lot of explanation and qualification. The reality could be shorter or much longer, particularly for individual cases.

Working with the models did impress a few overall conclusions on me. One: the estimated visa wait time differential between Rural and High Unemployment for India and China increasingly flattens as backlogs increasing depend on accessing Unreserved visas. Two: The market-favored “3-5 year” EB-5 visa wait time estimate looks vanishingly probable, at least in Rural and High Unemployment for China and India, even assuming optimized access to Unreserved visas. Given the sheer number of people who appear to be currently in process, not to mention ongoing demand, I can’t get my calculators to conclude moderate wait times for China and India in HUA or Rural — unless I start entering (what I consider) quite extraordinary assumptions about extra visa supply and/or applicant attrition. (Though not to say that the extraordinary is impossible, in these strange days.) The balance of probability looks to be on the side of greater-than-five-year visa wait times.

Infrastructure Outlook

[3/6 UPDATE: Thank you to the reader who emailed to notify me of two large Infrastructure projects not on my list. It now appears that over 400 Infrastructure investors may have been recruited by the end of 2025, meaning a multi-year backlog already in place in the Infrastructure category. See the Infra tab in my EB5 Backlog Analysis file for such detail as I’ve been able to find on infra projects, and email me if you can contribute any corrections or additional detail.]

What about the infrastructure category? In the last data release through July 2025, USCIS reported zero Infrastructure I-526E filed ever, not to mention zero petition approvals or denials. That must be a database glitch, as I’ve since confirmed reports of a few infrastructure I-526E filed before July 2025. But still, anecdotal evidence suggests that Infrastructure activity is recent and low-volume to date.

Based on the infrastructure project information that I can find from the Internet and by talking to people, I gather that 100 to 200 infrastructure investors may have been recruited by the end of 2025, and that over 1,000 infrastructure project slots are contemplated by the end of 2026. (See the Infra tab in my EB5 Backlog Analysis file for such detail as I’ve been able to find on infra projects, and email me if you can contribute any corrections or additional detail.)

For the investor from China or India, the recent activity means a tantalizing chance to be among the first <400 infrastructure visa applicants (in which case, clear path to a green card before the initial Infrastructure visa limit is reached and triggers the Visa Bulletin). On the other hand, the investor with an early 2026 priority date has no guarantee of ending up among the first wave of visa applicants. Even the earliest investors have no guarantee of snagging the first visas because I-526E processing and visa processing are not quite FIFO. And once Infrastructure demand collects and advances sufficiently to trigger country caps, Infrastructure supply suddenly becomes potentially tiny to China and India.

With supply so small – about 400 visas in the first year and 200 visas in subsequent years – the demand/supply imbalance can potentially go from 0x to 10+x very quickly. If every Infrastructure investor has to take an Infrastructure visa, then the China-born or India-born investor in 2026 faces a realistic chance of anywhere from zero visa wait time to a multi-decade wait time, depending on where he or she happens to sort out in the flurry of petitions coming in around the same time, and ongoing demand from Rest of World investors. On the other hand, assuming access to Unreserved visas, I assume that Infrastructure investors today are — at worst — no worse off than Rural and High Unemployment investors with the same priority date. Since country and priority date theoretically determine access an Unreserved visa, no matter if the investment was in a Rural, HUA, or Infrastructure project. Also, many Infrastructure projects also qualify in High Unemployment or Rural, further diversifying visa options.

Process Factors

My big picture analysis looks at applicants in the aggregate, assuming that groups proceed in order according to the distinguishing features of priority date, TEA category, and country of origin. The reality is not so tidy, and individual experience can vary widely.

Looking around in 2026, I note developments related to the confusing issue of who gets advanced when and why in the EB-5 process.

As of today, there appear to be more processing barriers in consular processing than status adjustment. There appears to be better opportunity for litigation to affect timing in the U.S. Applicants who happen to be currently based in the U.S. may, at least for awhile, enjoy a timing advantage over fellow-countrymen abroad with the same priority date.

The new I-526E inventory management approach now explicitly considers set-aside visa usage, which can result in changes going forward to processing order. I-526E processing in 2024/2025 varied over a wide range of dates, with a few people getting very quick processing times (and thus early chance at a visa) while others waited. I guess that those variations may be about to decrease.

I’ll guess that Mandamus actions, which may explain a lot of individual processing time difference in 2024/2025, have decreasing opportunity/effectiveness going forward for I-526E and visa issuance. Considering the new inventory management guidance, the sheer numbers now awaiting I-526E processing and visa issuance, and impending Visa Bulletin dates. I-956F timing should also have a decreasing effect on investor petition timing, as a greater proportion of the I-956F inventory has now been processed. But I-526E processing order, for good or ill, retains potential to help determine who gets a visa and and when independent of the priority factors that are supposed to control visa allocation.

Visa Bulletin Outlook vs Backlog Outlook

The long-term risk of visa wait times and retrogression follows the difference between total applicants in the pipeline as compared with visa availability in coming years. (When I say “pipeline visa applicants,” I mean everyone who’s started the process by filing I-526/I-526E and who doesn’t have a green card yet, regardless of where they are in processing.)

By contrast, the near-term risk of Visa Bulletin cut-off dates follows from the difference between currently-qualified visa applicants and visa availability/usage this year. (When I say “qualified visa applicants,” I refer to the subset of the pipeline who currently have I-526/I-526E approval and visa applications complete, ready and waiting for the visa interview/adjustment and visa number assignment.)

As of early 2026, we appear to remain in the situation where set-aside categories have many pipeline applicants but few qualified applicants. (Refer again to the tables copied above for detailed estimates from approval data vs receipt data.)

If trends as of early 2025 continued, then there just haven’t been enough I-526E approvals in HUA or Infrastructure yet to create sufficient applicants yet for FY2026 visas. (This may be about to change, as the I-526 inventory management change may spur more HUA and Infra processing.) If lacking qualified applicants for available visas, no wonder the Visa Bulletin keeps showing “current.” This is a total guess on my part (in absence of any 2026 data yet), but (betting on government dysfunction) I would be surprised if High Unemployment gets Visa Bulletin dates this year, and (considering recent demand) astonished if Infrastructure gets Visa Bulletin movement this year. [3/6 UPDATE: I have now been notified of a flurry of Infrastructure approvals in recent months, making Visa Bulletin movement for Infrastructure at least not impossible this year.]

Rural is more dicey for the Visa Bulletin, because a continuation of 2025 USCIS processing trends would’ve resulted in more than enough Rural approvals and qualified visa applicants by now to use FY2026 visas. No dates or warnings yet in the Visa Bulletin for Rural makes me infer that despite having applicants ready and waiting, Department of State is not yet on track – for its own processing reasons — to issue all the 4,000+ Rural visas available in FY2026. If consulates are continuing to move as slowly as last year on set-aside applicants, then there’s no need for the Visa Bulletin to step in and control visas that aren’t being issued anyway. I hope – for the sake of wait times long term – that visa issuance volumes will increase enough to justify Visa Bulletin dates for Rural shortly. But I won’t be very surprised if that doesn’t happen.

If FY2026 ultimately passes without any Visa Bulletin cut-off dates in EB-5 set-aside categories, that’s good for the concurrent filing window, good for anyone who wants to lie that backlogs don’t exist until announced in the Visa Bulletin, and bad for wait times in the long term because it reflects deferred backlog advancement and lost visas.

More Information

If you’d like to discuss specific visa and timing questions one-to-one, my paid timing consultation service remains available. You can book a Zoom meeting through my scheduler. (And if the payment or time zone options don’t work for you, email suzanne@lucidtext.com and I can set you up with an alternative.)

If you benefit from everything I share with the writing and spreadsheets, please consider making a contribution to support the research, thinking, and time behind them. I have Paypal and Stripe links available. This is really a lot of work, on the side of my regular business plan writing service, and the blog is uncompensated except when a few readers step in with support. I appreciate it!