How long does USCIS take to process EB-5 petitions and applications? We have two sources of data relevant to the processing time question: the IPO Processing Time report, which indicates the filing date of petitions currently being processed, and the Forms Data Page, which gives data for the number of received, approved, denied, and pending petitions by quarter. The first source is helpful for past petitioners, while the second source can be better for current/prospective petitioners estimating future processing times.

IPO Processing Time Report

Every month, the USCIS Processing Time Information page updates a chart titled “Average Processing Times for Immigrant Investor Program Office” that looks like this.

What does this chart mean?

What does this chart mean?

The single unambiguous function of this report is to indicate when petitioners may begin to complain. A stakeholder email from USCIS in January 2017 explained,

We post case processing times on our website as a guide for when to inquire (service request) about a pending case. For the last several years, we have posted case processing times using two different formats: For cases that were within our production goals, we listed processing times in weeks or months; For cases that were outside of our production goals, we listed processing times with a specific date.

Always refer to your I-797C, Notice of Action, and look for “receipt date” to determine when we accepted your case. If the receipt date on the USCIS Processing Times web page is after the date we have listed on your notice, you should expect to hear from us within 30 days. If after those 30 days, you have not heard from us, you may make an inquiry on your case. We recommend using our e-request tool for all case inquiries.

With this in mind, the table can be read to mean “As of November 30, 2016, we were processing at least some I-526 cases filed as of August 7, 2015. If your I-526 petition was filed before 8/7/2015 and you haven’t heard from us, you may start making inquiries.”

The processing report also allows a general conclusion that the I-526 processing time for investors with an August 2015 priority date was 16 months (November 30, 2016 – August 7, 2015 = 16 months). (Though we know of people who filed I-526 in August 2015 and got earlier decisions or are still waiting, thanks to one or another exception to the first-come-first-served principle.)

The processing report indicates expected times for past petitioners up to a certain date. (I’ve logged processing times/dates for petitions from 2013 to 2015 in this spreadsheet.) The report does not say anything about the future. Since August 2015, IPO capacity has grown and EB-5 demand has grown even faster. The fact that an August 2015 petition had a 16-month processing time does not promise that a 2016 or 2017 petition will have the same time.

Petition Data

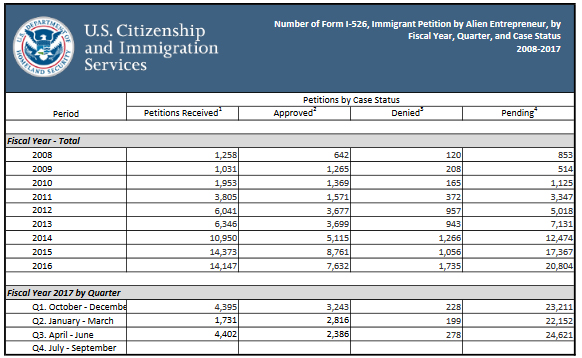

As a prospective EB-5 investor, or someone who filed I-526 in 2016 or 2017, I would look at form filing data to estimate future processing times. For example, see this chart of I-526 data from the USCIS Immigration Forms Data page:

This report provides information commonly used in waiting line models: inventory (pending petitions in the system), arrival rate (petitions received) and flow rate (approved + denied petitions, aka completion rate or throughput). For an example of how to use this data to make predictions with a simple waiting line model, see the Prediction tab of my I-526 times spreadsheet.

2019 UPDATE: I made an EB-5 Timing page to combine links to articles and resources related to petition processing and visa timing.