Priority date retention and redeployment, with flow chart

July 29, 2019 5 Comments

NOTE: The content of this post has been outdated since the EB-5 Immigrant Investor Program Modernization regulation was vacated in June 2021.

Among other changes, the new final rule for EB-5 Immigrant Investor Program Modernization “provides priority date retention to certain EB-5 investors.” This post (1) discusses context for this change, (2) summarizes the content of the change, and (3) provides a flow chart to illustrate the various options for changing course with an EB-5 investment.

Context Summary

Priority date retention is one small fix toward a major problem in EB-5: the mismatch between policy and reality when it comes to EB-5 timing.

The EB-5 at-risk policy and material change policy depend on a relatively short EB-5 process. An enterprise can be expected to sustain itself and keep EB-5 capital deployed for five years or so, and to closely mirror the original business plan predictions for a year or two.

But reality, for many investors, is a protracted EB-5 process with years upon years in which changes will inevitably occur. Projects will finish, loans will get repaid, plans may evolve, and problems may occur. The at-risk and material change policies are not flexible to accommodate such business developments over time. The longer the immigration process, the more vulnerable investors become to prohibited project-level changes or to difficulty in sustaining the investment at risk – and that despite having created jobs as required. A decade-long wait for a visa becomes particularly problematic when the visa depends on no material changes occurring with the investment over that period. Thus the need for options for good-faith investors who may find themselves, at some point over the years, needing their funds to be moved from one project to another.

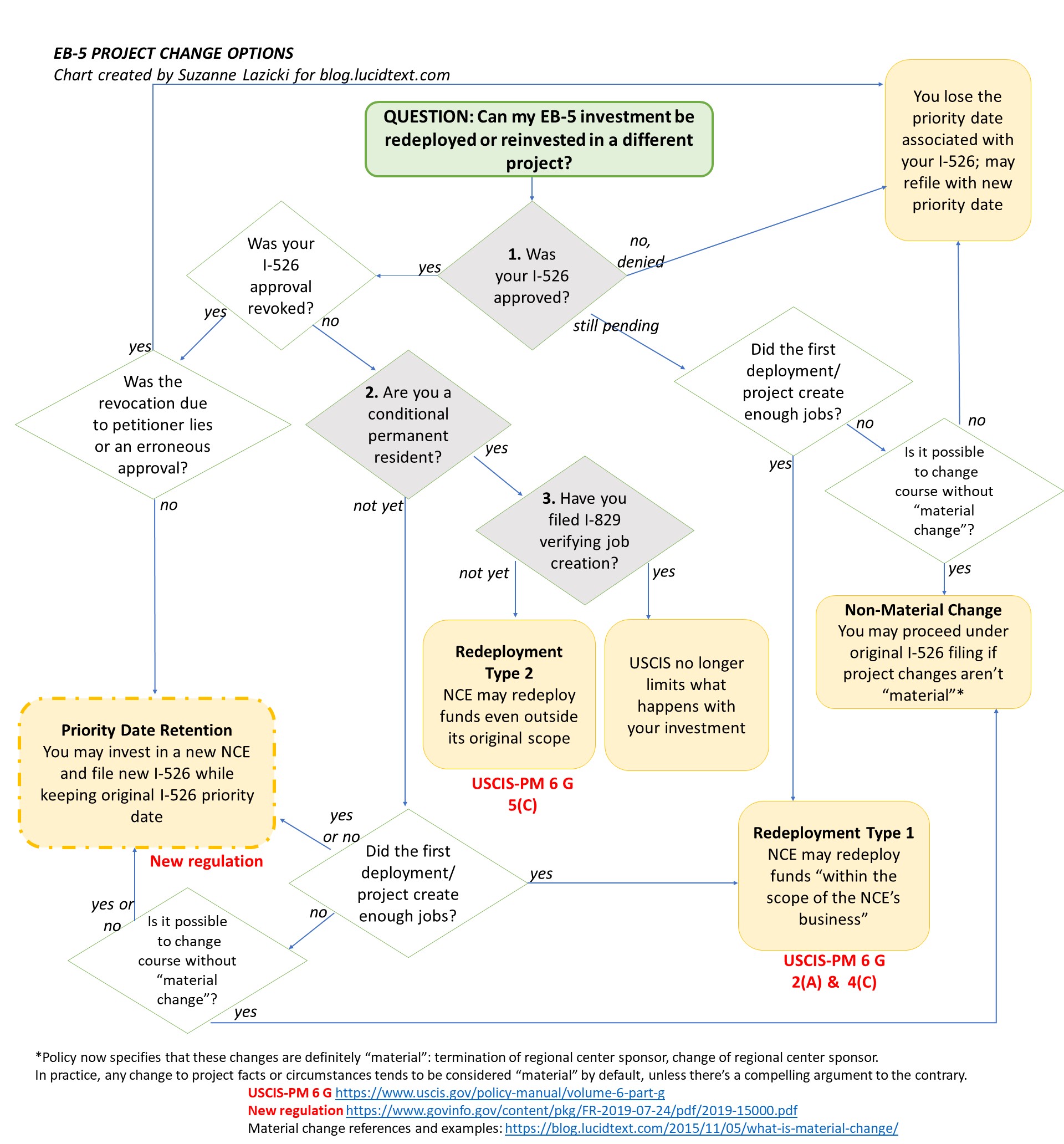

The “redeployment” policies are one attempt to accommodate change over time. The first redeployment policy, now described in Chapter 2(A) and Chapter 4(C) of the EB-5 section in the USCIS Policy Manual, creates some flexibility within the at-risk and material change requirements that apply to investors prior to conditional permanent residence. Moving EB-5 investment from one project to another would often be considered a fatal change at this stage, but Type 1 Redeployment defines a limited option for acceptable redeployment in a new project/use following completed job creation, within the scope of the enterprise’s business. The second redeployment policy, described in Chapter 5(C), recognizes even more flexibility in the at-risk and change policies that apply to investors once they have received conditional permanent residence. Type 2 Redeployment recognizes options for acceptable redeployment even before completed job creation, and even outside the scope of the enterprise’s ongoing business. While succeeding and getting repaid too early could be a fatal failure to sustain investment, Type 2 Redeployment policy offers a path to keep investment sustained.

The redeployment policies have not been well-loved (1) because everyone is confused by them (with many people not even noticing that there exist two distinct redeployment policies, and with not even USCIS able to explain the parameters), and (2) because the policies are a limited work-around, not a solution to the fundamental problems: excessively long wait times, and flawed underlying material change and at-risk requirements. “Redeployment” was at least intended to help by creating paths to accommodate some change. The flow chart at the base of this post illustrates the project change options introduced by redeployment policies, and the conditions under which they apply as described in the policy manual. Without redeployment policy, more arrows in the flow chart would lead to the “you lose” result box.

Priority date retention now introduces another limited work-around for investors who face losing the chance for a visa due to changes over the course of long waits. It’s especially helpful for one category of people excluded from the redeployment recourse: those whose regional center sponsor is terminated or changed while they are still waiting for a visa. These people still face I-526 revocation thanks to DHS’s faulty interpretation/application of material change policy. But at least, the new final rule provides them opportunity to salvage the priority date, saving the place in the visa queue in case they’d like to try again with a new I-526.

Content Summary: Priority Date Retention in the Final Rule

(All the answers in this section, except for my aside on data, come from the text of the Final Rule for EB-5 Immigrant Investor Program Modernization.)

What is priority date retention?

This provision of the Final Rule allows a petitioner to retain the priority date of an approved I-526 petition to use in connection with any subsequent I-526 petition filed by that petitioner.

Who are the “certain EB-5 investors” eligible to take advantage of priority date retention?

Eligibility for priority date retention applies to the population of people at any given time who meet all these conditions:

- The person is the petitioner on an I-526 petition that USCIS approved

- The person has not yet received an EB-5 green card (conditional permanent residence)

- If USCIS subsequently revoked the I-526 approval, it was for reasons other than (1) fraud or a willful misrepresentation of a material fact by the petitioner; or (2) a determination by USCIS that the petition approval was based on a material error

[Aside: DOS and USCIS statistics do not directly count this population. But to give a ballpark, I estimate that at least over 24,000 investors are currently in this window between I-526 approval and visa, and eligible to take advantage of the provision. Consider that no Chinese who filed I-526 after FY2014 has a visa yet per the visa bulletin, that there were about 35,500 China I-526 filed from FY2015-FY2018, that about 8,000 of those China I-526 were still pending at USCIS as of the end of FY2018, and that the approval rate for China I-526 has been about 90%. (Stats from my collection.) That’s already almost 24,000, and not counting the number of Vietnamese and Indian investors who are or will soon be stuck in that window thanks to retrogression. It’s another question what percent of this eligible population may be incentivized to take advantage of priority date retention. The most likely user: someone whose I-526 approval with an old priority date has been or is likely to be revoked, who comes from an oversubscribed country, and who has sufficient funds and immigrant intent to invest again in a new project at the new investment level.]

Clarifications in the final rule:

- The final rule becomes effective on November 21, 2019. Beginning on that date, eligible people may file a new I-526 while retaining the priority date from a previously-approved I-526. The rule specifies no restriction on when the previously-approved I-526 need have been filed. [9/30 UPDATE: Robert Divine said at the IIUSA conference that he also interprets no restriction on when the new I-526 can be filed — could be before 11/21.] “The changes in this rule will apply to any Form I-526 filed on or after the effective date of the rule, including any Form I-526 filed on or after the effective date where the petitioner is seeking to retain the priority date from a Form I-526 petition filed and approved prior to the effective date of this rule.”

- A priority date can only be transferred between one approved EB-5 petition and a subsequent EB-5 petition filed by that same petitioner. The priority date cannot be transferred between people (including, not to the investor’s spouse/dependents), and cannot be transferred to petitions for other visa categories.

- Priority date retention does not provide grandfathering under old rules. If someone chooses to file a new I-526 petition after November 21, 2019, he or she may keep the priority date of a previous I-526, but not the rules that applied that that previous I-526. The new I-526 filing will be subject to the increased investment amount and revised TEA provisions. “The regulatory requirements, including the minimum investment amounts and TEA designation process, in place at the time of filing the petition will govern the eligibility requirements for that petition, regardless of the priority date.”

- The priority date retention option depends on having an I-526 approval, and on not having an EB-5 visa. The commentary on the final rule explains why DHS thinks that filing I-526 is insufficient in itself to establish a priority date, and that people with an EB-5 visa do not need the priority date protection.

- The priority date retention option is available to victims of fraud by projects or regional centers. In fact, it was designed to help them. A petitioner is only excluded if an I-526 was revoked due to fraud by the petitioner.

- The final rule does not require NCEs to facilitate investors who wish to make a change. Nor does it change the EB-5 “at risk” requirement. That is to say, the rule does not change the difficulty of salvaging capital from one investment and moving it to another. The rule simply reduces the pain of starting over by allowing petitioners to at least salvage the old priority date if they choose to make a new investment and new I-526 filing

- DHS does not care how many I-526 you file. No matter how many priority dates you have for EB-5 petitions, you can use the oldest one associated with an approved petition when claiming a visa.

- The final rule specifies that it does not make any change to application of the Child Status Protection Act. The rule does not explain, if a petitioner had multiple I-526 petitions, which petition’s pendency gets subtracted from the child’s age at the time of visa availability.

- The final rule does not consider the question of how USCIS would treat a situation where the investor files a new I-526 after 11/21 in the same NCE/same project for which he had an approved I-526 from before 11/21. This situation could arise for someone whose I-526 approval was revoked only for loss of regional center sponsor, though the project was/is viable. So long as the original $500,000 was sustained in the NCE, presumably it would counted toward the investment amount required for the new I-526. But what if some of the initial capital had been lost/misappropriated — does it all still count in the new I-526 filing? Or what if the project had no particular use for the additional investment the investor would be required to make under the new minimum investment amounts — at least no use related to job creation? Maybe people drafting the rule just assumed that new I-526 would be based on fresh investments in new projects. At any rate there’s no guidance for situations in which the investor may be trying to salvage his or her original investment, original project, and original job creation as well as the original priority date.

Flow Chart

Considering that redeployment (as described in the USCIS Policy Manual) and priority date retention (as described in the final rule) are a maze of if-then statements, I’ve attempted a picture worth a thousand words. The flow chart image highlights several points that are often forgotten in discussions about redeployment: the existence of different redeployment options/requirements at different stages, and the pivotal questions of material change and whether or not the initial deployment already met the job creation requirement. (This chart matches my careful reading of the Policy Manual. But lawyers please email me with references if you see anything that does not match your reading, and I may update the image.)

References:

USCIS Policy Manual https://www.uscis.gov/policy-manual/volume-6-part-g

New Regulation: https://www.govinfo.gov/content/pkg/FR-2019-07-24/pdf/2019-15000.pdf

Material change references and examples: https://blog.lucidtext.com/2015/11/05/what-is-material-change/