RC Designation and Terminations, SEC (Palm House), RC List Updates

August 5, 2018 9 Comments

Regional Center Terminations

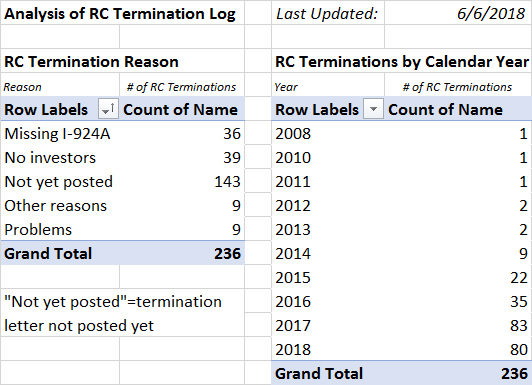

USCIS has now posted notices for regional centers terminated through March 2018, and I’ve added them to my termination log. Now we know the reasons behind about two thirds of the 250 regional center terminations to date.

USCIS has framed its activity in terminating regional centers as an integrity measure, but in fact only 11% of terminations so far have been due to integrity problems. The majority of terminations have been because (1) the regional center has not secured EB-5 investment in the past three or more years, and/or (2) USCIS did not receive the regional center’s Form I-924A annual report and fee on time for the most recent year.

The letters themselves are interesting for discussion of a topic not fully explained by the regulations or policy: what does it mean to promote economic growth? What must a regional center do, exactly, to justify its continued existence? How can the definition of “failure to promote economic growth” be stretched to cover the various reasons USCIS might want to terminate a regional center in practice?

A few noteworthy letters from the most recent batch posted on the USCIS website:

- Some might see Lansing Economic Development Corporation Regional Center as a model of regional center worth: the economic development agency of a distressed city using EB-5 as a tool in its economic development toolkit. This development agency reported that it promoted the EB-5 option in multiple trips to India, China, Italy, and throughout Europe, and offered EB-5 as an option to all development projects in Lansing. However, USCIS found that “While these activities are necessary for the continued operation of any regional center in the EB-5 Program, it does not show that the Regional Center has engaged in activities that promote economic growth as understood under the EB-5 Program. Specifically, these actions have not resulted in increased export sales, improved regional productivity, job creation, or increased domestic capital investment in the Regional Center’s designated geographic area.” Whatever its promotional activities, the regional center had not yet secured any EB-5 investment, and its potential projects did not include a shovel-ready project certain to use EB-5 investment. Therefore “USClS concludes that the Regional Center no longer serves the purpose of promoting economic growth.”

- Live in America-Midwest Regional Center is an example of an as-yet inactive regional center that’s part of an active network. USCIS issued the RC a Notice of Intent to Terminate for three years of I-924A that did not report any EB-5 investment. The Regional Center countered by pointing to successful projects sponsored by other regional centers in the Live in America network, arguing that this demonstrates LIA’s proven ability to get projects done, and potential to promote economic growth in the regional center geography. The RC indicated that is exploring and actively seeking investment opportunities, has met with EB-5 project candidates, and has entered into strategic partnerships. USCIS responded that the RC cannot rely on evidence of projects outside its approved geographic area, and that the future plans described are merely “future aspirational goals,” and do not count as “actually engaged in the promotion of economic growth.” Having an operator that’s been demonstrably successful in promoting economic growth did not save Live in America-Midwest Regional Center from termination. Sorry, Minnesota! The Midwest has had any regional centers at all thanks in part to serial regional center operators who can afford to give low-profile geographies a chance because they also have feet in New York and California. But USCIS appears less willing to give the Midwest a chance. Attract EB-5 investors within three years (or at least, get term sheets and file an I-924 amendment) or thy regional center designation shall be terminated.

- Charlotte Harbor Regional Center is a cautionary tale of what can happen when a regional center does not have copies of documents submitted by its investors to USCIS in I-526 petitions.

- USCIS terminated Greater Houston Investment Center, LLC for inactivity, and declined what seems to me a sensible request: the option to reactivate designation if a project opportunity presents itself in the future.

- America’s Regional Center was terminated in 2017 for lack of activity (no investors in 3 years), but was restored on July 5, 2018 to the list of approved regional centers. No appeal has been published, so I don’t know how the RC overcame the termination decision.

- Powerdyne Regional Center‘s mistake was to hire a President who turned out to be a wanted man in China.

- These regional centers presented USCIS with evidence of EB-5 projects in the pipeline, but USCIS argued that the projects were insufficiently advanced or showed insufficient commitment to EB-5 financing. Liberty South Regional Center, EB5 Memphis Regional Center, LLC, North Country EB-5 Regional Center, LLC, Guam Strategic Development Regional Center, Immigration Funds, LLC

- New Orleans Mayors Office of Economic Development got a 36-page termination notice that fits six termination reasons under the general umbrella of failure to serve the purpose of promoting economic growth. These are: lack of activity (only one project since 2008, and no new job creation/investment since 2013), lack of progress in the construction of the regional center’s one project, doubt about the legitimacy and viability of the portfolio business model used, material misrepresentations that cast doubt on the regional center’s legitimacy (Form I-924A reports that were inconsistent with each other and evidence that USCIS determined independently), improper use of EB-5 capital that casts doubt in investor’s ability with EB-5 requirements, and diversion of EB-5 funds (outside of the regional center geography, and inconsistent with the job creation purpose). Generally the termination comes as no surprise, since the New Orleans Mayor’s Office made the mistake of hiring operators for their regional center who proceeded to loot investor funds (or so alleged investors as early as 2012 and the Department of Justice in 2018). USCIS did not consider the Mayor’s suggestion that her office might continue to use EB-5 as a tool for job creation and growth in New Orleans under a different operator. The decision includes this paragraph that reads like policy, though it’s not written elsewhere,

- The reasons why a regional center may no longer serve the purpose of promoting economic growth are varied and “extend beyond inactivity on the part of a regional center.” 75 FR 58962. For example, depending on the facts, a regional center that takes actions that undermine investors’ ability to comply with EB-5 statutory and regulatory requirements such that investors cannot obtain EB-5 classification through investment in the regional center may no longer serve the purpose of promoting economic growth and may subvert a purpose of Section 610(a)-(b) of the Appropriations Act, which provides for regional centers as a vehicle to concentrate pooled investment in defined economic zones by setting aside visas for aliens classified under INA 203(b)(5). Likewise, a regional center that fails to engage in proper monitoring and oversight of the capital investment activities and jobs created or maintained under the sponsorship of the regional center may no longer serve the purpose of promoting economic growth in compliance with the Program and its authorities.

Most of the termination letters have little discussion, but appear to reflect a simple bright line: you didn’t attract an EB-5 investor in three years and thus are not promoting economic growth and lose your designation. This line can look reasonable, but I also see it threatening the regional center program’s basic potential as an economic tool. Consider that according to a list of investor petition approvals by regional center (briefly published by USCIS in June 2017), only 328 out of around a thousand regional centers had had one or more I-526 adjudicated from 2014 to 2017. Of those 328 regional centers, the majority were located in New York, California, Florida, Washington D.C., Atlanta, Chicago, Seattle, or Texas. If USCIS keeps terminating every regional center that’s not immediately popular with investors and active projects, the program will soon be left with few regional centers (and thus little opportunity to use the program) outside New York, California, Florida, Washington D.C., Atlanta, Chicago, Seattle, and Texas. That certainly wouldn’t match Congressional intent for economic impact. And how does it even benefit USCIS? How much would it cost USCIS to keep the generally blameless Economic Development Corporation of Lansing, Michigan on the list of regional centers, even if that RC doesn’t have EB-5 investors yet? (On the other hand, this position paper on regional center terminations makes the case that inactive RCs burden the system and are incompatible with the RC program as defined.)

SEC Action

The SEC has announced its first EB-5 fraud action this year: Securities and Exchange Commission v. Palm House Hotel LLLP, et al., No. 9:18-civ-81038 (S.D. Fla. filed August 3, 2018). The SEC is rather late to the party, following United States of America v. Robert V. Matthews and Leslie R. Evans (3/14/2018) and a civil suit filed by EB-5 investors in 2016. (Though not as late as USCIS, which has not terminated the regional center involved even as it hustled to terminate Lansing EDC.) The allegations are familiar: misappropriation of investor funds by people who arranged to have unfettered access to those funds. I note that the SEC’s list of defendants is much shorter than the list of defendants in the complaint by investors. The SEC identifies the regional center principals as responsible for misrepresentations, while investors also felt misled by the consultants and service providers involved.

Processing Times

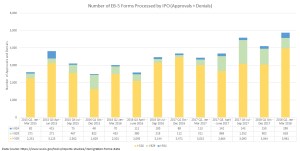

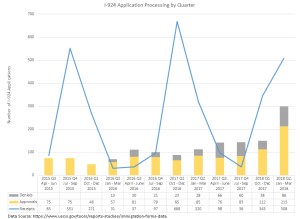

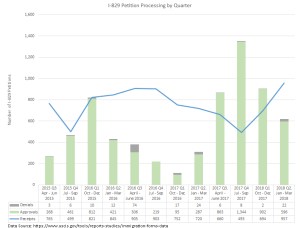

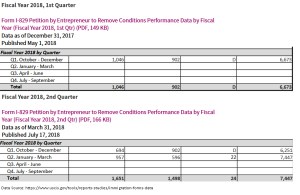

USCIS updated the Processing Times page on August 1, with improvements for all EB-5 forms (-23 days for I-526, -5 days for I-829, and -63 days for I-924).

Washington Updates

As I hear anything new on the Yoder amendment with potential to remove per-country limits for EB-5, I add it to my previous post. Not that I have heard much. Since the explosion of conflicting comment on my post, perhaps others in EB-5 have learned better than to make statements on this topic. (Update: IIUSA has finally made a comment.) I guess that response has also been complicated by the difficulty of reading the amendment text; it appears that even Yoder and the House appropriations committee may not have initially understood what was actually in it. I hear that my reader comments are being noticed and appreciated, and I hope that those comments help inform discussions among the powers that be.

I keep an eye on www.reginfo.gov just in case EB-5 regulations should proceed after all to the review stage in time to be finalized in August 2018. But nothing there yet.

Regional Center List Changes

Additions to the USCIS Regional Center List, 7/16/2018 to 08/02/2018

- Cypress Regional Center LLC (California)

- Liberty Harbor Regional Center LLC (Connecticut, New Jersey, New York, Pennsylvania)

- Lighthouse Regional Center, LLC (Texas)

- My Life Atlanta Regional Center, LLC (Georgia)

- Rise Investment Management, LLC (Connecticut, New Jersey, New York)

- Tinian EB-5 Regional Center, LLC (Commonwealth of Northern Marianas Islands)

New Terminations

- Northeast Ohio Regional Center (Ohio) Terminated 7/18/2018

- Nevada Development Fund LLC (Nevada) Terminated 7/12/2018

- Americas Green Card Regional Center (Maine, Massachusetts, New Hampshire) Terminated 7/12/2018

- Chicagoland Foreign Investment Group (CFIG) Regional Center (Illinois, Indiana, Michigan, Minnesota, Wisconsin) Terminated 7/16/2018

- EB5 United West Regional Center, LLC (California) Terminated 7/27/2018

- Fairhaven Capital Advisors American Samoa Regional Center Corp. (American Samoa)

- Cal Pacific RC LLC (California) Terminated 7/16/2018